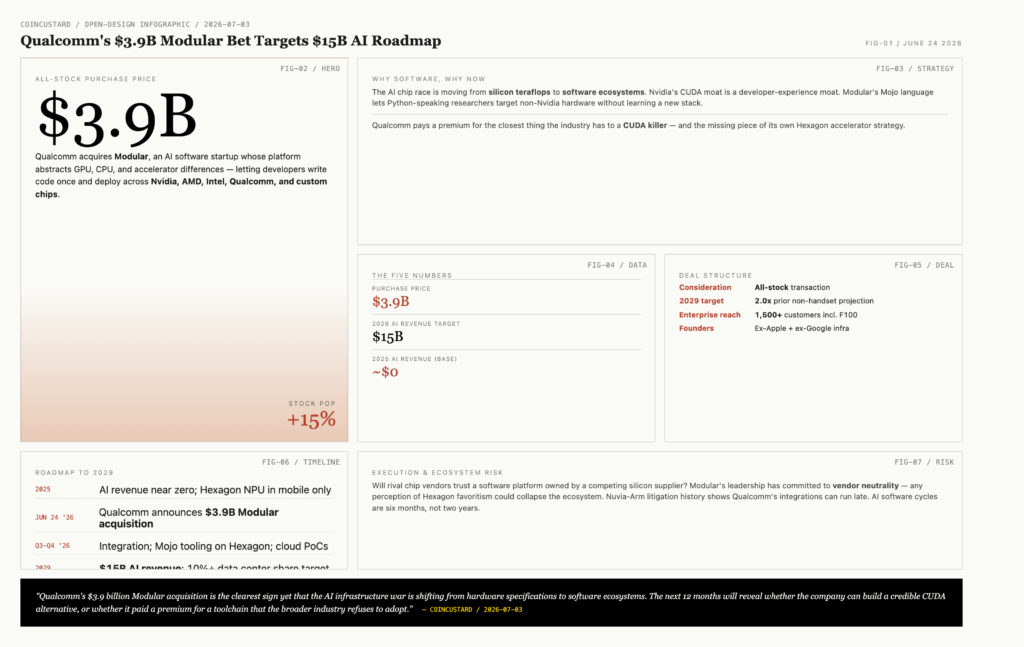

Qualcomm has agreed to acquire Modular, an AI software startup whose tooling helps developers run machine learning workloads across heterogeneous hardware, in a $3.9 billion all-stock transaction that marks the chip giant’s most aggressive bet yet on the software layer of the artificial intelligence stack. The deal, announced on June 24, 2026, positions Qualcomm to challenge Nvidia’s near-monopoly on AI developer mindshare at exactly the moment the industry is searching for alternatives.

Modular’s platform abstracts away the differences between GPUs, custom accelerators, and traditional CPUs, letting model authors write code once and deploy it across Nvidia, AMD, Intel, Qualcomm, and proprietary chips without rewriting. That portability is the missing piece in the AI infrastructure puzzle, where today’s developers write CUDA-specific kernels for Nvidia hardware and then face months of porting work to reach any other vendor. Qualcomm is paying a premium for the company because that abstraction is the closest thing the industry has to a CUDA killer.

Why Qualcomm Is Paying $3.9 Billion for Software

Qualcomm’s stock popped 15 percent on the news, and analysts quickly framed the acquisition as the company’s pivot from a smartphone chip vendor in slow secular decline to an AI infrastructure company with a credible data center story. The San Diego-based company has spent the last three years building AI accelerators under the Hexagon brand, but adoption outside mobile has been slow because developers lack the tooling to target the chips efficiently. Modular’s software stack solves that problem.

Internally, Qualcomm has communicated a roadmap that takes AI-related revenue from effectively zero in 2025 to roughly $15 billion annually by 2029, a target that requires capturing meaningful share of the data center and edge AI markets that Nvidia currently dominates. The Modular acquisition is the single largest piece of that plan. Without a software abstraction layer, the company’s excellent hardware was trapped behind a fragmented developer experience, a fate that befell every AI chip startup of the last cycle.

The Five Numbers That Define the Deal

- $3.9 billion: the all-stock purchase price for Modular, the largest pure-software acquisition in Qualcomm’s history.

- $15 billion: Qualcomm’s internal target for AI-related revenue by 2029, up from a near-zero base in 2025.

- 15 percent: the single-day stock pop Qualcomm shares logged on the announcement.

- 2.0x: the multiplier on Qualcomm’s previously disclosed 2029 non-handset revenue projection, which the company roughly doubled inside a single quarter.

- 1,500+: the number of enterprise customers Modular claims to support, including several Fortune 100 banks and pharmaceutical companies.

Shifting the Chip War From Hardware to Software

For most of the last decade, the AI chip race has been a hardware race measured in teraflops, memory bandwidth, and HBM stack height. Nvidia won that race decisively with the H100 and the upcoming Blackwell generation, leaving AMD, Intel, and a long list of startups fighting for single-digit market share. The Modular deal signals that the next phase of the competition will be decided by software ecosystems rather than silicon alone, a field in which Qualcomm has historically been strong because of its mobile developer relationships. The founders, who previously built infrastructure at Apple and Google, designed the platform around Mojo, a Python-superset language that removes the single biggest barrier to non-Nvidia adoption: forcing AI researchers to learn a new language.

Competitive Pressure and Customer Questions

Qualcomm will need to answer a critical question from enterprise customers: does owning Modular give Qualcomm an unfair advantage in AI software, and will rival chip vendors continue to build on a platform owned by a competing silicon supplier? Modular’s leadership has committed to keeping the platform vendor-neutral, and the company’s existing relationships with AMD, Intel, and several cloud providers depend on that neutrality being maintained. Any perception of favoritism toward Qualcomm’s own Hexagon accelerators could collapse the ecosystem overnight.

The other major risk is execution. Qualcomm’s integration history is mixed. Its prior acquisition of Nuvia, a CPU design firm, produced the Snapdragon X Elite laptop chip but ran into protracted litigation with Arm over license terms, delaying the product by nearly two years. The Modular integration will need to move faster because the AI software market is moving in six-month cycles, not two-year ones. Missed release windows in this category can erase a year’s worth of competitive positioning in a single quarter.

What Comes Next for Qualcomm and the Broader AI Market

If the integration succeeds, Qualcomm’s combination of custom AI silicon plus a portable software layer becomes the most credible challenger to Nvidia’s CUDA moat. If it fails, the company will have spent $3.9 billion on a toolchain that its competitors either refuse to use or rapidly clone. The market will know which outcome is unfolding within four quarters, because either Modular’s customer count expands materially as enterprises adopt the cross-vendor abstraction, or it stalls as developers wait to see whether Qualcomm plays fair with rival hardware customers.

For Nvidia, the deal is a strategic warning shot. The hardware giant has spent the last three years arguing that CUDA’s installed base is an unbreakable moat, and the Modular acquisition is the first credible attempt to commoditize that moat by selling portability rather than fighting performance spec-for-spec. Even if Qualcomm’s own AI chips capture only 10 percent of the data center market by 2029, the existence of a viable software alternative to CUDA changes the negotiating leverage of every cloud provider and every enterprise buyer. The chip war has moved from silicon to software, and Qualcomm just placed the largest single bet on the new battlefield.