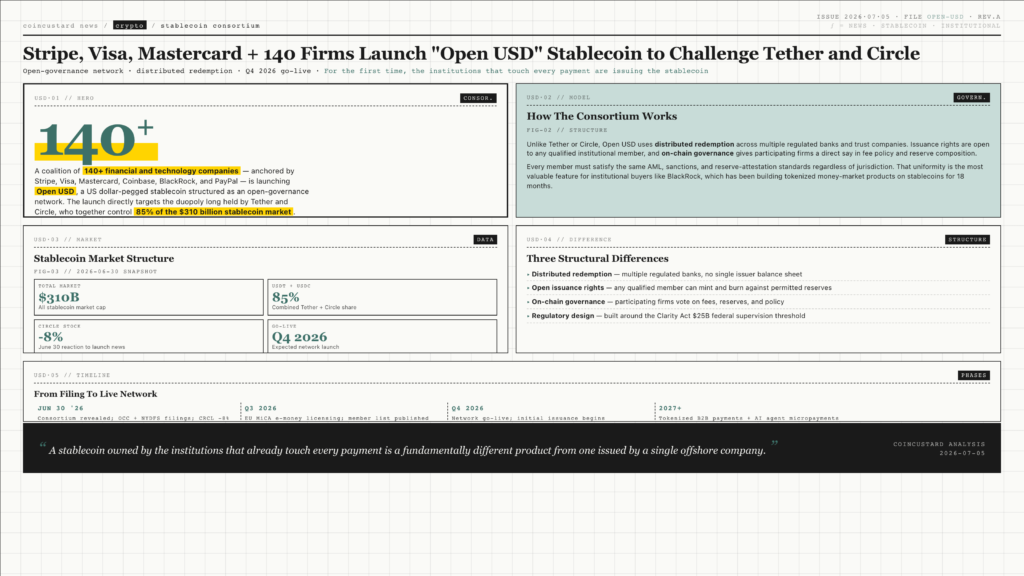

A coalition of more than 140 financial and technology companies, anchored by Stripe, Visa, Mastercard, Coinbase, BlackRock, and PayPal, is launching a new US dollar-pegged stablecoin that explicitly targets the duopoly long held by Tether and Circle. The consortium, revealed in regulatory filings and press reports on June 30, 2026, will operate under the working name “Open USD” and is structured as an open-governance network rather than a single corporate issuer. The timing is pointed: Tether’s USDT and Circle’s USDC together account for roughly 85 percent of the $310 billion stablecoin market, and the new entrant wants a slice of that flow before the next regulatory regime settles in Washington and Brussels.

Why A Consortium Stablecoin Matters

The Open USD model differs from a Tether- or Circle-style model in three structural ways. First, redemption and reserve custody are distributed across multiple regulated banks and trust companies rather than concentrated in one issuer’s balance sheet, addressing a long-standing complaint from bank treasurers. Second, issuance rights are open: any qualified institutional member can mint and burn Open USD against permitted reserves, which compresses settlement times and lowers spreads. Third, on-chain governance gives participating firms a say in fee policy and reserve composition, a feature Circle has so far declined to expose publicly for USDC.

The consortium has already filed paperwork with the Office of the Comptroller of the Currency and is in active dialogue with the New York Department of Financial Services. Compliance is the central design constraint: every member must satisfy the same anti-money-laundering, sanctions, and reserve-attestation standards regardless of jurisdiction. For a buyer like BlackRock, that uniformity is the most valuable feature; the asset manager has spent the last eighteen months building tokenized money-market products on top of stablecoins, and its preference is for a rail that can be plugged into every regulated venue in parallel.

Who Is In, And What It Costs

The launch lineup spans the full financial stack. Card networks (Visa, Mastercard), payment processors (Stripe, PayPal, Adyen), exchanges (Coinbase, Robinhood, Kraken), asset managers (BlackRock, Fidelity, Franklin Templeton), banks (JPMorgan, Bank of New York Mellon, Standard Chartered, SBI), and technology firms (Shopify, Salesforce, Snowflake) have all confirmed participation. The membership list will be published when the network goes live, expected in the fourth quarter of 2026.

The market reaction was immediate. Circle’s stock fell more than 8 percent on June 30 as analysts at Jefferies, Barclays, and Bernstein downgraded near-term USDC growth assumptions. Tether, privately held, did not comment, but on-chain flows showed USDT liquidity thinning on several Asian exchanges in the days that followed.

For the first time, a US-anchored stablecoin is being designed by the institutions that historically underwrote Tether’s and Circle’s customers.

The Regulatory Angle

Open USD lands as the SEC, the OCC, and the Federal Reserve are jointly drafting the first comprehensive US stablecoin framework. The Clarity Act, which cleared committee in late June, would require monthly reserve attestations, capital buffers, and federal supervision for any issuer above a $25 billion circulation threshold. The Open USD consortium has publicly endorsed those provisions, and the structure of its governance was built around them. That positioning is unlikely to be a coincidence: the group is offering Washington a compliant template in the hope of fast-tracked approvals and a head start on distribution.

For the European Union, the picture is messier. The Markets in Crypto-Assets Regulation, or MiCA, took full effect in 2024 and treats dollar stablecoins as electronic money tokens, subjecting them to e-money licensing in the country of issuance. Several consortium members have MiCA licenses already; others are racing to obtain them. Until those licenses are in hand, Open USD will be available in the EU only through partner e-money institutions, a constraint that will slow retail uptake but not prevent institutional use.

What It Means For Crypto Markets

Stablecoins sit underneath roughly $310 billion of crypto trading volume every twenty-four hours and are the working cash of most centralized and decentralized exchanges. The arrival of a third major USD option, especially one with card-network rails, is likely to compress the spreads between USDC and USDT and to bring new use cases into scope. Cross-border B2B payments, tokenized fund settlements, and AI-agent micropayments have all been cited by consortium members as priorities. If even a small share of the $150 trillion global B2B payments market shifts to Open USD, the resulting float could exceed the combined reserves of Tether and Circle within three years.

For now, the open question is execution. Building compliant rails across more than forty jurisdictions is a multi-quarter project, and the consortium’s track record on coordination is untested. But the strategic logic is hard to dispute: a stablecoin owned by the institutions that already touch every payment is a fundamentally different product from one issued by a single offshore company. The duopoly is being tested.