Nvidia is offering a new generation of AI startups something it has historically refused: a piece of the upside. Under a program disclosed to Bloomberg on July 1, 2026 and confirmed by CNBC, the Santa Clara chipmaker will swap blocks of compute capacity on its Blackwell and Rubin GPU clusters for revenue participation agreements — equity-style stakes in customer companies whose valuations scale with the AI infrastructure they consume. The shift, Nvidia’s most significant commercial departure from a pure hardware sales model in a decade, is designed to lock in the next wave of foundation-model builders at a moment when the AI infrastructure buildout has begun to outrun the capital reserves of even well-funded startups.

Bloomberg’s report, corroborated by sources at two early-participating startups and by Investor’s Business Daily on July 2, describes the program as a “compute-for-revenue-share” framework. Startups that commit to multi-year consumption of Nvidia’s neocloud capacity through partners like Sharon AI, Firmus Technologies, CoreWeave, and Lambda receive preferential GPU allocation in exchange for warrants, revenue participation rights, or direct equity that vest as the customer scales. Nvidia retains the right to take cash settlement in lieu of equity, and the warrants are structured to dilute only after a specified revenue threshold is met.

Why Now

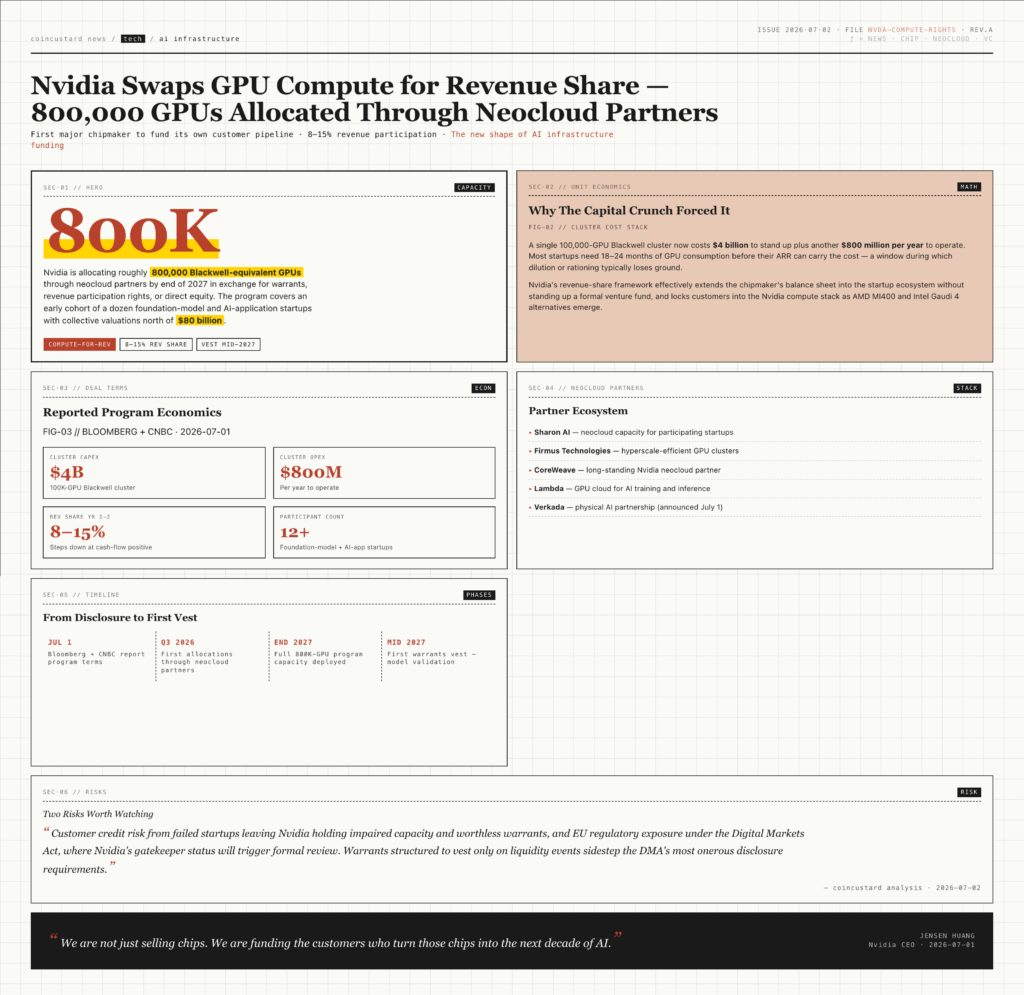

The timing is not accidental. The AI infrastructure buildout has accelerated faster than the venture capital model can fund it. A single Blackwell cluster scaled to 100,000 GPUs now costs upward of $4 billion to stand up and another $800 million per year to operate. Even with aggressive revenue assumptions, a typical foundation-model startup needs 18 to 24 months of GPU consumption before its own ARR can carry the cost — a window during which most startups have historically been forced to either dilute heavily or ration capacity and lose ground to better-capitalized competitors.

Nvidia’s revenue-share program effectively extends the company’s balance sheet into the startup ecosystem without the formal structure of a venture fund. It also locks customers into the Nvidia compute stack at a time when AMD’s MI400 series, Intel’s Gaudi 4, and a handful of custom silicon efforts from Google, Amazon, and Microsoft are beginning to offer credible alternatives. By tying the customer’s success to Nvidia’s own revenue participation, Nvidia converts what would otherwise be a commodity infrastructure sale into a long-duration partnership.

The Numbers

- Estimated program capacity: 800,000 Blackwell-equivalent GPUs allocated through neocloud partners by end of 2027.

- Reported early participants: a dozen foundation-model and AI-application startups, with collective valuations north of $80 billion.

- Neocloud partner ecosystem: Sharon AI, Firmus Technologies, CoreWeave, Lambda, and Verkada among the publicly disclosed counterparties.

- Typical deal economics: 8% to 15% revenue share in years one and two, stepping down as startups reach cash-flow positive.

“We are not just selling chips. We are funding the customers who turn those chips into the next decade of AI.” — Jensen Huang, Nvidia CEO, July 1, 2026

Risks And Complications

The revenue-share model introduces a category of risk Nvidia has not previously carried: customer credit risk. If a startup funded through the program fails to reach the revenue thresholds required to amortize the GPU consumption, Nvidia’s books absorb the loss in the form of impaired capacity and worthless warrants. The company has signaled that it will reserve against these exposures quarterly, in line with its existing inventory and accounts-receivable practices, but analysts expect meaningful volatility in Nvidia’s services and other revenue line as the program ramps.

Regulatory exposure is a second concern. The arrangement shares characteristics with a venture investment, and Nvidia’s auditors are likely to require consolidation or equity-method accounting for the larger participations. In the European Union, the program will require review under the Digital Markets Act because of Nvidia’s gatekeeper status for accelerated computing. Nvidia’s legal team has reportedly structured the warrants so they vest only on liquidity events, sidestepping the DMA’s most onerous disclosure requirements.

What It Means For The AI Stack

For startups, the program is unambiguously positive. A startup that previously faced a binary choice between heavy dilution and slow scaling now has a third path: trade a slice of long-tail upside for the compute runway needed to actually build the product. For the broader AI ecosystem, the program creates a tier of well-capitalized challengers that can compete with OpenAI, Anthropic, and Google DeepMind without immediately ceding equity to traditional VCs. That, in turn, increases the supply of foundation models and applied AI products in the market — a long-term tailwind for adoption that Nvidia is happy to fund because every additional successful customer deepens the moat around its compute stack.

The first warrants under the new program are expected to vest in mid-2027, by which point Nvidia will have a year of operating data to assess whether the model produces the durable, high-margin services revenue the company has been promising Wall Street. If it does, expect every other AI infrastructure vendor — from AMD to the hyperscalers — to copy the framework within twelve months. If it does not, Nvidia will have run an experiment whose losses are absorbed in a quarter that the company’s $3 trillion market cap can easily afford, and the rest of the industry will move on.