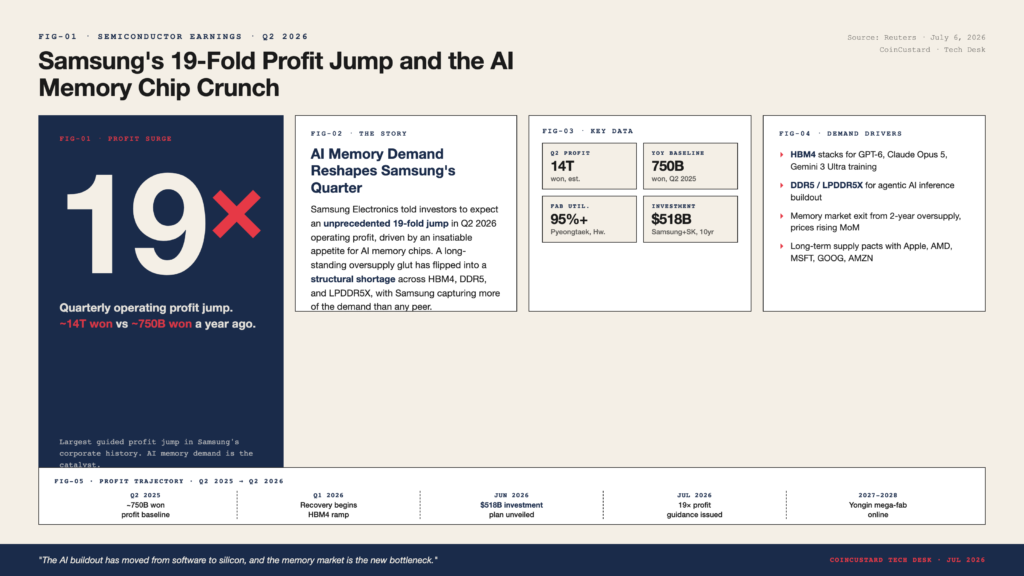

Samsung Electronics has told investors to expect a 19-fold jump in quarterly operating profit, the strongest guidance in the company’s history, driven by an insatiable appetite for AI memory chips that has turned a long-standing oversupply glut into a structural shortage. The forecast, reported by Reuters on July 6, 2026, confirms that the AI buildout has become the single most important demand driver for the global memory market, and that Samsung is capturing more of that demand than any of its competitors.

The guidance implies an operating profit of roughly 14 trillion won for the quarter, up from approximately 750 billion won a year earlier. The magnitude of the swing is unprecedented for a company of Samsung’s size and reflects a combination of rising prices for high-bandwidth memory, an industry-wide capacity expansion that has not kept pace with AI-driven demand, and a meaningful share gain against rival SK Hynix, which had been the dominant supplier of HBM3E and HBM4 to Nvidia and the major hyperscalers.

What Is Driving the Surge

Three factors are converging. First, the training runs for the latest generation of frontier models, including GPT-6, Claude Opus 5, and Gemini 3 Ultra, require memory bandwidth that can only be delivered by HBM4 stacks, a product category where Samsung was late to qualify but is now ramping aggressively. Second, the inference buildout for agentic AI systems is driving demand for high-capacity DDR5 and LPDDR5X modules, where Samsung holds the largest market share. Third, the broader memory market has emerged from two years of oversupply, and contract prices for DRAM and NAND are now rising month over month.

The capacity picture is particularly tight. Samsung’s memory fabs in Pyeongtaek and Hwaseong are running above 95 percent utilization, and the company’s Xi’an and Suzhou packaging facilities are operating around the clock. The constrained supply has given Samsung unusual pricing power, with several major customers, including Apple, AMD, and the hyperscaler trio of Microsoft, Google, and Amazon, signing long-term supply agreements that lock in volumes and prices through 2028.

The $518 Billion Investment Plan

Samsung’s profit surge is also a vindication of the company’s $518 billion investment commitment, announced jointly with SK Hynix in late June, to build out AI-focused chip capacity in South Korea over the next decade. The plan, which includes a new mega-fab in Yongin, advanced packaging facilities in Cheonan, and a research center in Giheung, will increase Samsung’s total wafer capacity by roughly 40 percent by 2030 and add dedicated HBM and AI accelerator lines that are expected to come online in 2027 and 2028.

The investment is one of the largest private sector capital commitments in Asian industrial history and has been framed by Seoul as the centerpiece of South Korea’s national AI strategy. The Korean government has matched the private commitment with tax incentives, expedited permitting, and a new visa category for foreign semiconductor engineers, all of which are designed to lock in Samsung and SK Hynix’s lead over Chinese competitors such as YMTC and CXMT, both of which remain years behind on HBM technology.

What It Means for Nvidia, Apple, and the Hyperscalers

For Nvidia, Samsung’s ramp is good news. The AI chip leader has been the primary beneficiary of the memory crunch through its H200 and B200 products, both of which require HBM3E or HBM4 stacks. Samsung’s qualification as a second source for HBM4, alongside SK Hynix and Micron, reduces Nvidia’s single-supplier risk and gives the company leverage in pricing negotiations. Apple, which uses Samsung memory across its iPhone, iPad, and Mac lines, is also benefiting from the long-term supply agreements, which insulate it from the spot price spikes that have hurt smaller customers.

The hyperscalers face a more complex picture. Microsoft, Google, and Amazon have all committed to multi-billion-dollar AI infrastructure buildouts for 2026 and 2027, and the memory cost is a meaningful share of the total. Higher memory prices translate directly into higher capex, which has already shown up in the latest quarterly results from all three. The flip side is that the memory crunch validates the AI capex cycle, suggesting that the demand is real and structural rather than speculative.

Risks and Watchpoints

Three risks could derail Samsung’s trajectory. First, a faster-than-expected ramp from Chinese memory makers, particularly CXMT, could compress pricing in the DDR5 segment within 18 months. Second, a shift in AI architecture away from transformer-based models toward more memory-efficient designs could reduce HBM demand. Third, a broader economic slowdown could reduce consumer demand for the smartphones, PCs, and servers that consume the bulk of Samsung’s memory output.

Samsung’s management addressed all three in its guidance call, arguing that the AI demand cycle is durable, that the architectural shift to memory-efficient models is still years away, and that the consumer recovery is intact. The 19-fold profit jump is the company’s strongest vote of confidence in that thesis, and the next two quarters will be the test of whether the bet pays off.

The Bigger Picture

Samsung’s earnings preview is the clearest signal yet that the AI buildout has moved from software to silicon, and that the memory market is the new bottleneck. The 19-fold profit jump is not a one-off: it is the first of several quarters in which AI memory demand is expected to dominate corporate earnings across the entire semiconductor supply chain, from Samsung and SK Hynix at the memory layer to Nvidia, AMD, and Broadcom at the compute layer to TSMC at the foundry layer. The chip crunch is no longer coming. It is here.