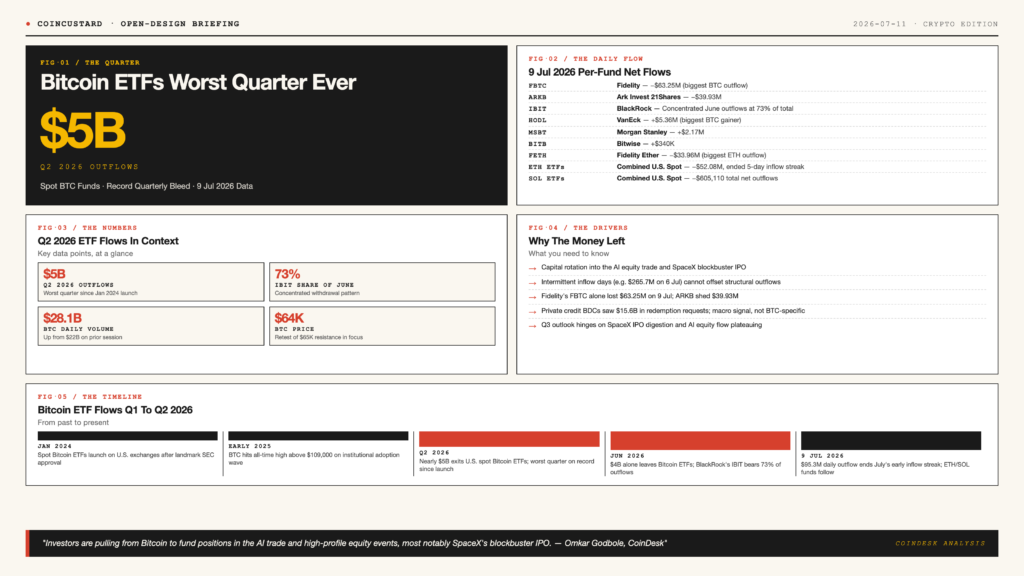

U.S. spot Bitcoin exchange-traded funds just closed their worst quarter since launch, with nearly $5 billion in net outflows in the second quarter of 2026, a record quarterly bleed that has reshaped the institutional posture toward the original crypto asset. The withdrawal, documented in fresh SoSoValue data, accelerated sharply through June and has continued into early July, even as Bitcoin’s price staged a partial recovery above the $64,000 mark.

The second quarter is now the worst stretch for Bitcoin ETF flows since the products debuted in January 2024, a roughly 30-month run during which the funds had become the dominant on-ramp for institutional and retail investors seeking regulated exposure to the asset. The reversal marks a notable shift in sentiment among the asset managers and family offices that helped drive Bitcoin to its all-time high above $109,000 in early 2025.

IBIT Bore the Brunt

BlackRock’s IBIT, the largest spot Bitcoin ETF by assets under management, accounted for roughly 73 percent of June’s $4 billion in monthly outflows, an unusually concentrated withdrawal pattern that has prompted fresh scrutiny of the fund’s institutional client base. According to data compiled by CoinDesk analyst Omkar Godbole, the pace of withdrawal from IBIT accelerated through the second half of June and into early July, suggesting that the selling pressure is being driven by a small number of large holders rather than broad retail rotation.

On July 9 alone, U.S. spot Bitcoin ETFs shed a combined $95.3 million, ending a string of strong days earlier in the month. Fidelity’s FBTC led the daily outflows with a $63.25 million withdrawal, followed by Ark Invest’s ARKB, which lost $39.93 million. VanEck’s HODL bucked the trend as the day’s biggest gainer, adding $5.36 million, while Morgan Stanley’s MSBT and Bitwise’s BITB posted smaller inflows of $2.17 million and $340,000 respectively.

“Investors are pulling from Bitcoin to fund positions in the AI trade and high-profile equity events, most notably SpaceX’s blockbuster IPO.” — Omkar Godbole, CoinDesk

Ether and Solana Funds Follow

Selling pressure spread beyond Bitcoin. U.S. spot Ethereum ETFs recorded $52.08 million in combined net outflows on July 9, ending a five-day streak of positive flows. Fidelity’s FETH accounted for the largest single Ethereum withdrawal at $33.96 million, though the fund has still accumulated roughly $2.147 billion in cumulative net inflows since launch. Combined net assets across all U.S. spot Ethereum ETFs stood at $9.345 billion as of mid-July.

Spot Solana ETFs also paused after several days of gains, with combined outflows of $605,110 as some investors locked in profits. The relatively modest size of the Solana withdrawals reflects both the smaller asset base of the funds and the comparatively limited institutional penetration of the Solana trade.

The Rotation Story

Analysts are increasingly framing the Q2 outflows not as a Bitcoin-specific capitulation but as a deliberate rotation into competing opportunities with clearer near-term catalysts. CoinDesk reports that the primary driver has been capital reallocation toward the artificial intelligence trade and high-profile equity events, most notably the blockbuster initial public offering of SpaceX, which has absorbed billions in institutional demand since pricing.

That framing matters for interpreting the data. These are not panic redemptions triggered by Bitcoin-specific bad news, but rather calculated repositioning by investors who see higher expected returns elsewhere. The implication is that the outflows could reverse quickly once the SpaceX IPO and the broader AI equity trade lose momentum, returning capital to the Bitcoin complex.

A Macro Signal Worth Watching

Bitcoin ETFs occupy the most liquid end of the digital asset investment spectrum, exchange-traded products that can be exited in seconds during regular trading hours. The simultaneous stress in private credit business development companies, where redemption requests surged to $15.6 billion in the second quarter and exceeded the 5 percent quarterly cap at 10 of 16 monitored BDCs, suggests that the outflow pattern is part of a broader macro shift in risk appetite rather than a Bitcoin-specific phenomenon.

When structurally unrelated vehicles see simultaneous liquidity rushes, the correct interpretation is almost always macro-level rather than asset-specific. Investors across multiple asset classes are reaching for cash at the same time, and the convergence is the signal worth watching rather than any single fund’s daily flow.

Bitcoin traded above $64,000 in early Friday action with daily volume spiking to $28.1 billion, up from $22 billion the previous day, a sign that the early July rebound has not yet attracted the institutional bid needed to absorb the Q2 outflows. Whether the SpaceX IPO completes its digestion in the coming weeks, and whether AI equity flows begin to plateau, will likely determine whether Q3 brings a return of ETF inflows or a continuation of the record-breaking withdrawal pattern that defined Q2 2026.

What Q3 Is Likely to Bring

Several indicators will help frame the next phase of the institutional Bitcoin trade. Spot Bitcoin ETF net inflows on July 6 reached $265.7 million, one of the strongest single days in weeks, suggesting that the bid for regulated exposure has not disappeared entirely. The challenge for Q3 is whether those intermittent inflow days can be sustained long enough to offset the underlying structural rotation toward AI equities and mega-cap IPOs.

Fitch’s warning on private credit redemption gates adds another layer of caution. When investors simultaneously seek liquidity in products that are designed to be illiquid, the dynamic can compound, forcing fund managers to sell underlying positions at discounts and accelerating the redemption cycle. That dynamic, if it spills from private credit into adjacent asset classes, would be a far more worrying signal than any single quarter’s Bitcoin ETF outflows.

For now, the Bitcoin market is operating in a holding pattern: spot price above the psychologically important $60,000 level, ETF flows marginally negative, and a broader macro backdrop that has not yet committed to either a sustained risk-on rally or a deeper pullback. The Q2 record outflows are a meaningful data point, but they remain a function of competing opportunities rather than a structural rejection of Bitcoin as an institutional asset class.