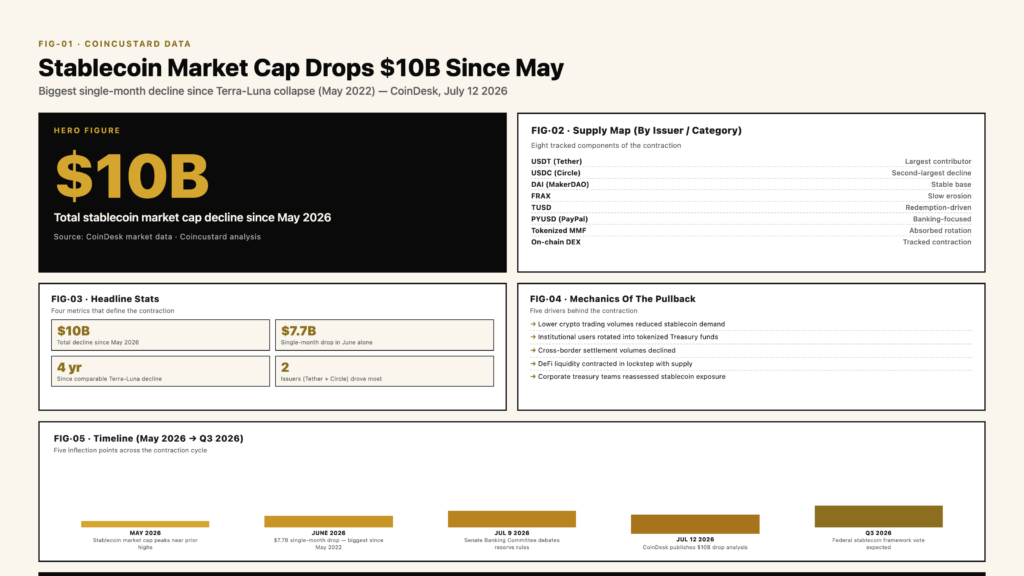

The stablecoin market has shrunk by roughly $10 billion since the start of May, with $7.7 billion of that contraction landing in June alone. According to data tracked by CoinDesk, the drawdown marks the largest single-month dollar decline in the sector since the Terra-Luna collapse of May 2022, when algorithmic stablecoins failed and triggered a multi-quarter credit event across digital-asset markets.

For years, stablecoins were treated as the quiet plumbing of the crypto economy: dollar-denominated tokens issued by Tether, Circle, and a handful of smaller firms, used to move funds between exchanges, settle trades, and provide a refuge during volatility. The recent contraction suggests that assumption deserves a second look, with both Tether’s USDT and Circle’s USDC contributing meaningfully to the slide even as institutional adoption of tokenized dollars continues to grow.

The Anatomy of a $10 Billion Pullback

The mechanics of the contraction are familiar from previous cycles but playing out on a much larger balance sheet. USDT supply has declined on net for two consecutive months, the first sustained reduction since the 2022 episode, while USDC has lost ground despite a wave of new banking and payments integrations. Analyst commentary published this week attributed the move to a combination of reduced trading activity on centralized exchanges, lighter demand for cross-border settlement, and a rotation by crypto-native funds into tokenized money-market funds and yield-bearing alternatives.

The numbers matter because stablecoins sit at the foundation of nearly every on-chain transaction. When their supply contracts, total addressable liquidity in the broader crypto market contracts with it. Several market-structure indicators, including open interest on perpetual futures and the volume of stablecoin pairs on major exchanges, have moved in tandem with the supply reduction since late spring.

Where the $10 Billion Went

- Reduced demand for stablecoins as crypto trading volumes cooled through June

- Rotation by institutional users into tokenized U.S. Treasury and money-market funds

- Net redemptions across the two largest issuers, Tether and Circle

- Lower cross-border settlement volumes from payment-rail partners

“Stablecoins are supposed to be neutral, but they behave like a risk asset when liquidity tightens.”

Why Analysts Are Not Panicking

Despite the headline number, the analyst community is largely treating the contraction as cyclical rather than structural. Demand for dollar-pegged tokens typically falls when speculative appetite dries up and recovers when it returns, and several on-chain indicators already point to stabilization in early July. Tokenized money-market funds, which have absorbed some of the rotation, have grown in lockstep with stablecoin redemptions over the same period, suggesting that the dollar is leaving crypto-native rails rather than leaving crypto entirely.

That distinction matters for the policy debate. Stablecoin issuers have spent the past two years pitching their products to U.S. and European regulators as essential infrastructure for payments, capital markets, and cross-border settlement. A $10 billion drop in supply, even one tied to a benign rotation, complicates that narrative. If regulators interpret the data as evidence that stablecoin demand is volatile and procyclical, the case for a comprehensive federal framework becomes easier to make and harder to defer.

The Legislative Backdrop

Both chambers of Congress have stablecoin legislation in active drafting, with the Senate Banking Committee and House Financial Services Committee working from competing drafts that would impose reserve, audit, and disclosure requirements on issuers. The recent contraction has been cited in committee discussions as evidence that the market cannot be left entirely to its own devices. Industry groups, including the issuing firms themselves, have endorsed a federal framework but argued that overly stringent reserve rules could push issuers offshore.

The Bigger Picture for Crypto Markets

Beyond the immediate policy debate, the contraction has knock-on effects for the rest of the digital-asset ecosystem. Centralized exchanges earn a meaningful share of revenue from stablecoin float and trading fees; decentralized finance protocols have built lending markets and automated market makers that assume a baseline level of stablecoin liquidity; and corporate treasury teams that have moved portions of their working capital into stablecoins are now confronting the fact that the instruments they chose for stability have not been entirely stable in practice.

What Issuers Are Doing About It

The two largest issuers have responded with different strategies. Circle has leaned into regulated banking and payment-rail partnerships, betting that institutional adoption will outlast any retail-driven contraction in supply. Tether has continued to expand its presence in emerging markets and in commodity trade finance, where its distribution network reaches users that traditional banking rails do not. Both firms have publicly maintained that they can meet redemption demand at par, and neither has disclosed meaningful liquidity stress in the most recent attestations.

Whether the contraction marks the end of a multi-year stablecoin growth story or simply a pause in it will depend on a handful of variables that should clarify by the end of the third quarter: the trajectory of crypto trading volumes, the pace of tokenized money-market fund adoption, the final shape of any U.S. federal framework, and the broader appetite for dollar-denominated digital assets among institutional allocators. For now, the $10 billion figure is the headline, but the underlying story is about how the plumbing of crypto responds when the cycle turns.