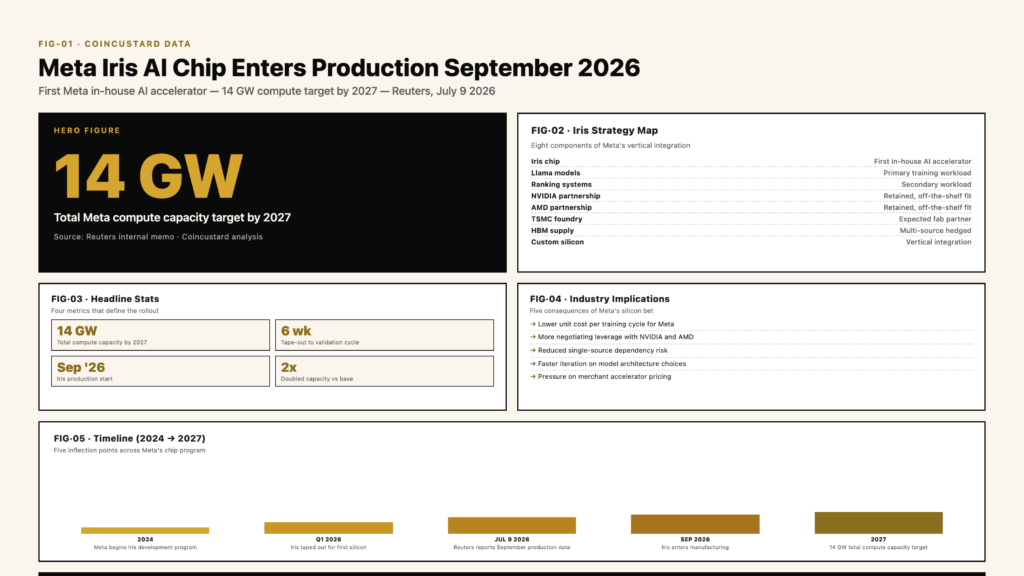

Meta Platforms plans to begin manufacturing its first in-house AI training chip, codenamed Iris, in September, according to an internal memo reviewed by Reuters. The move is the most concrete signal yet that the company is preparing to bring a meaningful share of its AI compute capacity in-house, with a stated goal of doubling total computing power to 14 gigawatts by 2027.

Iris passed testing in roughly six weeks, an unusually short cycle for a custom AI accelerator, and is now moving into production as Meta seeks to reduce its reliance on external suppliers and to lower the cost of training the next generation of its large language models. The chip is the centerpiece of a multi-billion-dollar infrastructure program that has become one of the largest capital expenditure lines in Meta’s history.

Why a Custom Chip, and Why Now

The economics of frontier AI have shifted decisively toward companies that can control their own compute stack. Training a state-of-the-art model today requires tens of thousands of accelerators running in coordinated clusters, and the per-chip cost, the per-watt cost, and the supply availability of those accelerators have become strategic variables. Meta’s bet is that a custom silicon path, layered on top of its existing partnerships with NVIDIA and AMD, gives the company more negotiating leverage, more control over its roadmap, and ultimately a lower unit cost for the compute that will power its AI products.

That bet has precedent in the industry. Google has been shipping its own Tensor Processing Units for more than a decade. Amazon’s AWS offers Trainium and Inferentia to cloud customers. Microsoft has worked with multiple partners on custom silicon. Until now, Meta has been a notable holdout, buying essentially all of its training capacity from external vendors. Iris changes that posture and signals that the company intends to operate more like a vertically integrated AI infrastructure provider.

The 14-Gigawatt Target

- Total compute capacity target: 14 gigawatts by 2027

- Iris production start: September 2026

- Testing cycle: approximately six weeks from tape-out to validation

- External suppliers retained: NVIDIA and AMD, alongside Iris

- Primary use case: training next-generation Llama models and internal ranking systems

“Iris is not a replacement for our partners. It is a second engine on the same aircraft.”

The Supply Chain Implications

Bringing a custom AI chip to production on a six-week testing timeline is a significant engineering achievement, but it leaves open the harder question of where the chip will be manufactured. Industry observers expect Iris to be fabricated by Taiwan Semiconductor Manufacturing Company, the foundry that produces the overwhelming majority of advanced AI accelerators. That dependency creates its own strategic exposure, particularly as U.S. and European policymakers push for more domestic semiconductor capacity and as trade tensions around Taiwan continue to weigh on capital planning across the tech sector.

Meta has not publicly disclosed Iris manufacturing partners, and the company’s capital expenditure disclosures suggest it is hedging across multiple suppliers rather than concentrating volume with any single foundry. That hedging posture is increasingly common among the largest AI labs, which have learned from recent supply shocks that single-source dependencies on advanced packaging and high-bandwidth memory can stall entire model roadmaps.

How Iris Compares to Existing Accelerators

Detailed specifications of Iris have not been disclosed, but industry analysts expect the chip to target training workloads specifically, with an emphasis on memory bandwidth and interconnect throughput rather than peak theoretical compute. That profile would align Iris with Meta’s largest internal workloads, which prioritize throughput on training clusters over latency-sensitive inference. The company has indicated that its existing partnerships with NVIDIA and AMD will continue to serve workloads where off-the-shelf accelerators remain the best fit, while Iris absorbs a growing share of internal training capacity.

What This Means for the AI Industry

Meta’s commitment to custom silicon is the strongest evidence yet that the hyperscale AI labs have moved past the experimental phase of accelerator design and into a period of structural vertical integration. The total addressable market for AI accelerators is large enough that custom chips will coexist with merchant silicon rather than displace it, but the negotiating leverage of the largest customers has clearly changed. NVIDIA, which remains the dominant supplier, now faces a customer base that increasingly has the engineering depth to design and ship its own alternatives.

The September production milestone will be the next concrete checkpoint. If Iris hits its targets on yield, performance, and cost, Meta is likely to expand the program and to bring forward the timeline on follow-on designs. If the chip underperforms expectations, the company will have the option to lean more heavily on its existing partnerships. Either outcome will reshape how AI labs think about compute, and how the chip industry plans for a future in which its largest customers are also its competitors. The downstream impact on cloud pricing, AI product margins, and the broader semiconductor supply chain will be felt long before any of those effects show up in earnings reports.