JPMorgan has delivered one of the most pointed warnings yet about the role Michael Saylors Strategy has come to play in the Bitcoin market. In a note circulated to clients this week and first reported by Bloomberg, the bank argued that Strategys evolving bitcoin sales policy introduces a new, avoidable, two-way risk into crypto markets at a time when liquidity is already thin and sentiment is fragile.

The note, written by JPMorgan strategists led by Nikolaos Panigirtzoglou, lands at an awkward moment. Strategy, the Tysons Corner, Virginia-based company formerly known as MicroStrategy, just disclosed a measured reduction in the pace of its bitcoin accumulation. That pivot, away from a years-long posture of buy at almost any price, was framed by Saylor as a response to a maturing balance sheet. JPMorgan reads it differently. The bank is warning clients that the very entity that helped institutionalize bitcoin as a treasury asset is now also the largest single source of incremental supply pressure on the market.

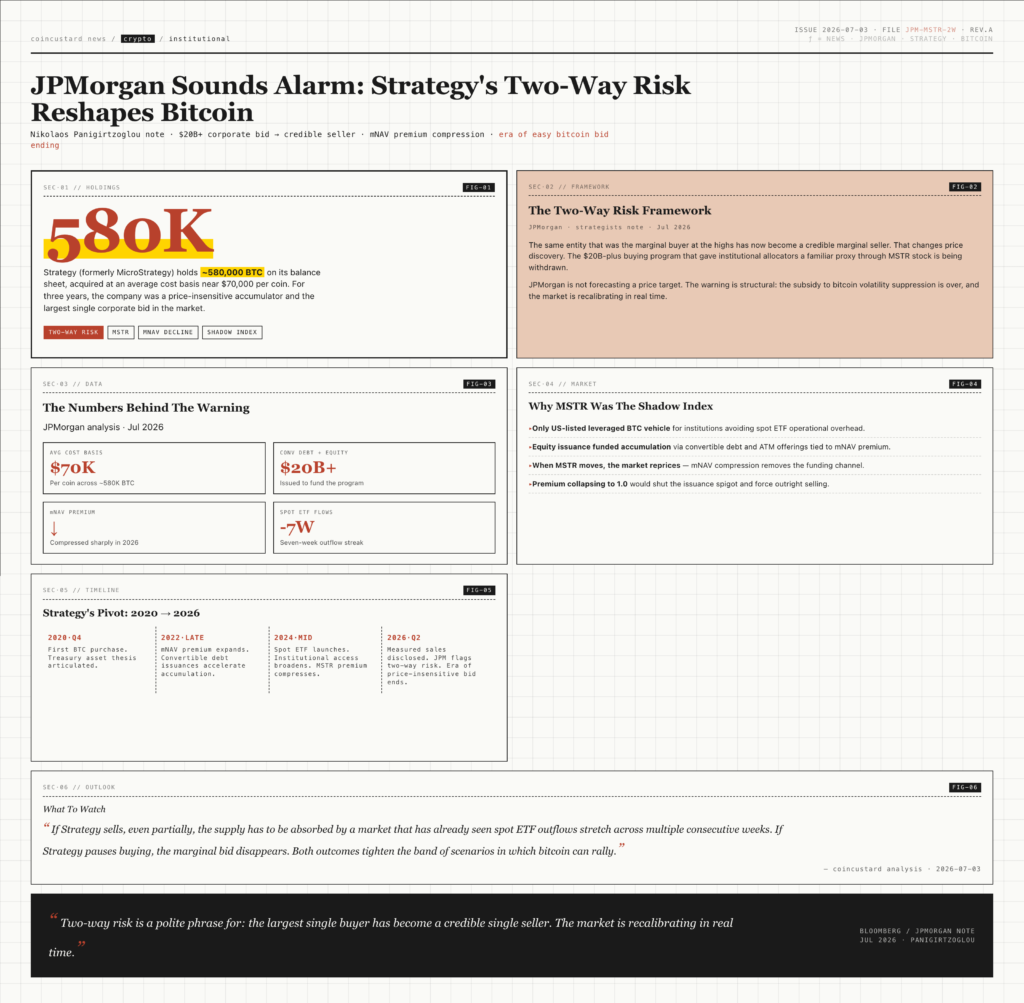

What JPMorgan Actually Said

The note is unusually direct by Wall Street standards. It argues that Strategys pivot introduces a two-way risk because the same entity that was the marginal buyer of bitcoin at the highs has now become a credible marginal seller. That changes the price discovery process. For most of the last three years, Strategy acted as a price-insensitive accumulator. Its $20 billion-plus buying program pulled coins out of circulation, supported futures curves, and gave institutional allocators a familiar proxy through MSTR stock. The JPMorgan team argues that this buying was, in effect, a subsidy to bitcoin volatility suppression.

With Strategy now signaling restraint, the subsidy is being withdrawn. Bitcoin is responding accordingly. Spot prices have spent the better part of June oscillating in a tightening range as the market digests the prospect of a future where the largest single corporate holder is no longer an automatic bid. JPMorgan does not forecast a price target in the note, but the language is a clear signal to clients that the structural floor under bitcoin is now lower than it was six months ago.

The Numbers Behind The Warning

- Strategy holds roughly 580,000 bitcoin on its balance sheet, acquired at an average cost basis near $70,000 per coin.

- The company has issued more than $20 billion in convertible debt and equity to fund its purchases, much of it at coupons and conversion prices that look stretched at current spot levels.

- MSTR shares trade at a premium to net asset value, a premium that has compressed sharply in 2026 as bitcoin has corrected from its late-2025 highs.

- JPMorgan estimates that the mNAV premium collapsing toward 1.0 would remove the equity issuance channel Strategy has used to fund its bitcoin strategy.

Why This Matters For The Broader Crypto Market

Strategys role in bitcoin markets has always been unusual. It is a publicly traded software company that converted itself into a leveraged bitcoin vehicle, with the share count, debt load, and corporate purpose all bent toward accumulating more coin. For institutional allocators, MSTR was the only US-listed way to get bitcoin exposure with leverage and without dealing with the operational headaches of a spot ETF. That made Strategy a kind of shadow index provider. When MSTR moved, the rest of the market was forced to reprice.

JPMorgan is now telling clients that this dynamic is becoming a liability. If Strategy sells, even partially, to manage its balance sheet, the supply has to be absorbed by a market that has already seen spot ETF outflows stretch across multiple consecutive weeks. If Strategy pauses buying, the marginal bid disappears and the futures curve flattens. Both outcomes tighten the band of scenarios in which bitcoin can rally.

Two-way risk is a polite phrase for: the largest single buyer has become a credible single seller. The market is recalibrating in real time.

The Saylor Defense And The Counter-Argument

Saylor, for his part, has spent the last week on media appearances and on X defending the new posture. He argues that selling a small fraction of holdings to cover operating expenses and to pay down the most expensive tranches of convertible debt is exactly what a maturing balance sheet is supposed to do. In his telling, the criticism from JPMorgan and from skeptics on crypto Twitter reflects a misunderstanding of corporate finance rather than a flaw in the bitcoin strategy itself.

The counter-argument, articulated by the JPMorgan team and echoed by analysts at several other large banks, is that the magnitude of the sales and the signaling effect matter more than the dollar amounts. A 5 percent trim of holdings is not large in absolute terms. It is enormous in terms of the message it sends to the marginal institutional allocator, who has spent the last three years assuming that Strategy would never sell at all. That assumption is now being walked back, and JPMorgan is arguing that the cost of unwinding it will be paid in higher volatility and a structurally weaker bid for bitcoin over the next several quarters.

What To Watch Next

The JPMorgan note is not a price call. It is a structural warning. The implications are clear: bitcoin is no longer being supported by a price-insensitive corporate accumulator, and the marginal supply has shifted in a way that institutional investors need to price in. The next 90 days will tell whether the market can absorb the policy change without a deeper drawdown, or whether the two-way risk JPMorgan flagged turns into a one-way repricing lower. Either way, the era of easy bitcoin bid is ending, and Wall Street has just put the change in writing.