The U.S. Securities and Exchange Commission is on track to unveil its first comprehensive cryptocurrency-focused regulatory framework in early-to-mid July 2026, an initiative dubbed Regulation Crypto that aims to establish conditional exemptions from standard securities registration requirements for specific digital asset activities. The package, flagged by SEC Chair Paul Atkins during a Tuesday update of the agency’s 2026 rulemaking agenda, is the most ambitious attempt yet by the federal government to put the U.S. digital asset industry on a permanent legal footing and ends three years of ad-hoc enforcement that critics on both sides of the debate said was holding the industry back.

At the heart of Regulation Crypto is a recognition that the SEC’s existing securities framework, written in the 1930s for paper-stock issuance, does not map cleanly onto software-based assets, decentralized protocols, or 24/7 trading venues. Atkins and his staff have spent the last several months drafting three parallel rulemakings designed to bridge that gap, and the agency plans to release the proposals for public comment as early as this month, with the goal of finalizing the most market-sensitive pieces before the end of the fiscal year.

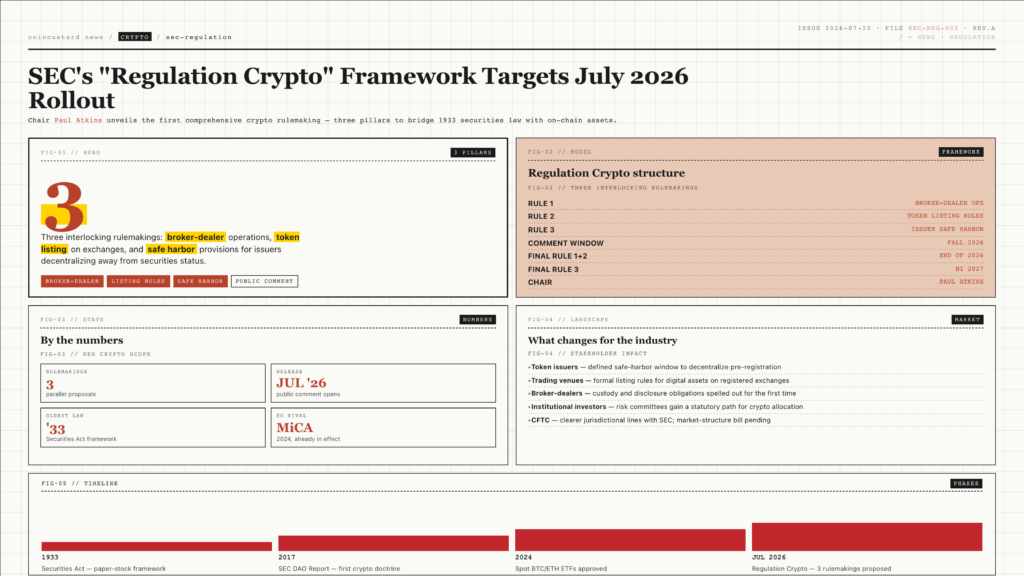

The Three Pillars of Regulation Crypto

The framework rests on three interlocking rulemakings, each addressing a distinct segment of the digital asset stack. The first pillar covers cryptocurrency broker-dealer operations, defining which platforms must register as broker-dealers, what custody rules apply to digital assets held on behalf of clients, and what disclosure obligations attach to retail-facing trading venues. The second pillar addresses how digital assets can be listed on trading platforms and national securities exchanges, a category that today includes the spot Bitcoin and Ethereum ETFs but that the SEC has so far refused to formally approve or reject for any token issued through a decentralized protocol.

The third pillar, and the one that has drawn the most attention from the industry, is a series of safe harbor provisions for token issuers transitioning away from acting as a traditional securities issuer. The safe harbor would create a defined window during which a project can decentralize, distribute tokens to a broad user base, and demonstrate functional network operations without triggering securities registration. If the issuer meets the criteria, the token graduates to a status that is regulated but not registered, a category that does not exist under the current securities code.

Why the Timing Matters

The July timing is not arbitrary. Congress is weighing several parallel crypto bills, including a comprehensive market-structure bill that would assign clearer jurisdictional lines between the SEC and the Commodity Futures Trading Commission. By publishing Regulation Crypto as a formal rulemaking proposal now, the SEC locks in its preferred framework before legislators can pre-empt it with a statute that the agency considers less friendly to market participants. The move also gives Atkins a concrete deliverable to point to as the commission’s signature contribution to the Trump administration’s stated goal of making the United States the preeminent global hub for digital asset activity.

That political context is not incidental. Atkins and his senior staff have been explicit that Regulation Crypto is designed to position the U.S. as the most attractive jurisdiction in the world for token issuers, exchange operators, and liquidity providers. The implicit competitor is the European Union, whose Markets in Crypto-Assets Regulation took effect in 2024 and which has already attracted a meaningful share of new token issuance. The implicit threat is a flight of capital and engineering talent to Singapore, the UAE, and Hong Kong, all of which have moved faster than the U.S. on retail-facing crypto frameworks.

This is the first time the SEC has put a comprehensive, written framework on the table for the digital asset industry. The proposal will be controversial. The fact that the proposal exists at all is the headline.

What Critics on Both Sides Will Say

Industry advocates will likely argue that the safe harbor’s decentralization thresholds are too vague, that the broker-dealer rules impose obligations that the largest platforms can absorb but smaller issuers cannot, and that the timeline for graduation from safe harbor to non-registered status is too long. Consumer-protection advocates are expected to push for stronger disclosure rules, mandatory segregation of customer assets, and stricter marketing restrictions on tokens that have not yet demonstrated functional decentralization. Both critiques have merit, and Atkins has signaled that the formal public comment period is intended to surface and resolve them.

For institutional investors, the most important practical effect of Regulation Crypto will be the legal clarity it provides for products that have so far been structured around enforcement assumptions rather than statutory authority. Spot crypto ETFs, tokenized money-market funds, and corporate treasury allocations to digital assets all depend on a chain of regulatory interpretations that could be reversed at any time. A formal rulemaking does not eliminate that risk, but it reduces it to a manageable level that institutional risk committees can underwrite.

What Happens Next

The next three months will determine whether Regulation Crypto becomes the foundation of a U.S. digital asset industry for the next decade or another iteration of an unfinished policy debate. The comment period for the three rulemakings will run through the fall, with the SEC under pressure from the administration to finalize at least the broker-dealer and listing rules before the end of 2026. The safe harbor is the more complex piece and is likely to take longer, with industry observers expecting final adoption in the first half of 2027.

For the broader crypto market, the proposal is the first credible signal that Washington intends to compete for the industry on rules rather than rhetoric. The companies that have spent three years building compliance programs in anticipation of exactly this moment are about to find out whether those programs are sufficient. The companies that have spent three years hoping regulation would never come are about to learn what compliance actually costs. Either way, the U.S. digital asset industry is about to get a legal shape it has never had before.