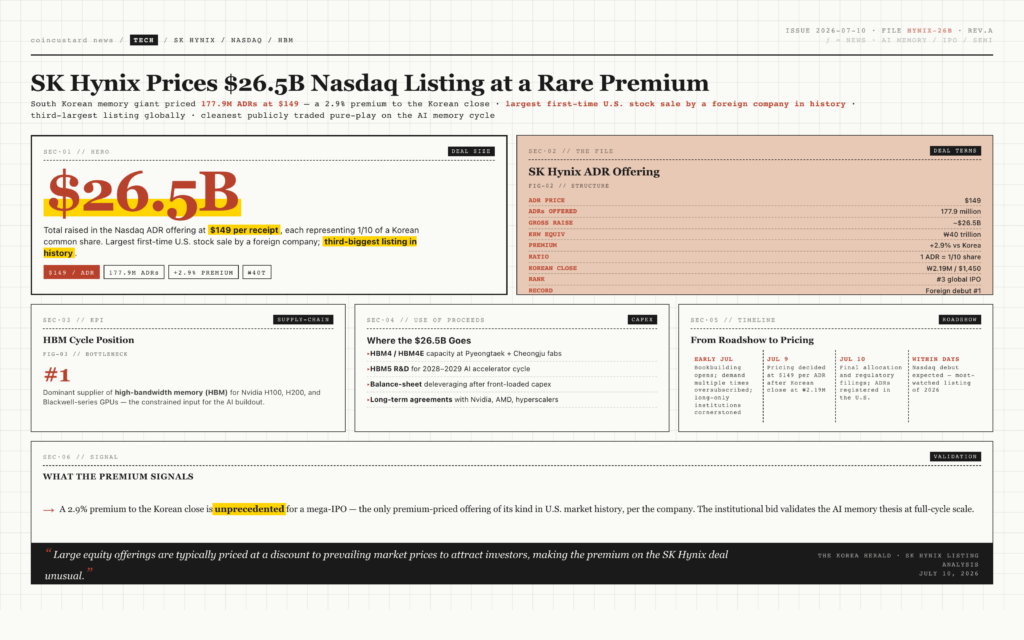

South Korean memory chipmaker SK Hynix has priced its blockbuster Nasdaq American Depositary Receipt offering at $149 per share, raising approximately $26.5 billion in what is now the largest first-time U.S. stock sale by a foreign company and the third-largest listing in global market history. The pricing, completed on Friday in Seoul, was set at a roughly 2.9 percent premium to SK Hynix’s closing price of 2.19 million Korean won, or about $1,450, on the Korean exchange the prior day, a rare and notable structure for a mega-IPO that has captured the attention of capital markets worldwide.

Under the terms of the deal, SK Hynix will offer 177.9 million ADRs in the United States, with each receipt representing one-tenth of a common share traded in Seoul. The structure is designed to give U.S. investors direct, liquid exposure to one of the world’s most important memory chipmakers, a company whose high-bandwidth memory products have become a bottleneck input for the global AI buildout. The deal is being marketed as the AI memory trade, the cleanest publicly traded pure-play on the HBM cycle.

Why a Premium Pricing Matters

Large equity offerings are almost always priced at a discount to prevailing market prices, both to attract cornerstone investors and to leave room for the stock to perform in the aftermarket. The 2.9 percent premium SK Hynix commanded is, by any measure, unusual. According to the company’s own marketing materials, this is the only premium-priced initial public offering of its kind in U.S. market history, a fact the lead bankers have leaned into heavily during the roadshow.

The premium signals extreme demand. Order books for the offering were multiple times oversubscribed, and the final allocation tilted heavily toward long-only institutional buyers, sovereign wealth funds, and dedicated AI-thematic funds. Retail participation was deliberately limited to avoid an unsustainable pop on the first day of trading. The pricing outcome is a direct vote of confidence in the AI memory cycle from the global institutional investor base.

The AI Memory Bottleneck

SK Hynix sits at the center of one of the most strategically constrained supply chains in the technology industry. The company’s high-bandwidth memory, or HBM, is the specialized DRAM stack used to feed Nvidia’s H100, H200, and Blackwell-series GPUs. Every leading AI training cluster and every frontier-model inference deployment needs HBM, and SK Hynix has, for the past eighteen months, been the dominant supplier. Samsung and Micron are now racing to close the gap, but the technology lead SK Hynix built is real and it is showing up in margins.

For investors, the appeal of the U.S. listing is straightforward. U.S. capital allocators have spent the last two years building positions in Nvidia, AMD, and the AI hyperscalers, and they have struggled to find a clean, liquid, pure-play way to get exposure to the memory layer underneath. SK Hynix, the only HBM vendor shipping in volume at the leading edge, has been the obvious target. The Nasdaq listing unlocks that position at scale.

How the Deal Compares to Other Mega-IPOs

At roughly $26.5 billion raised, the SK Hynix listing is the largest first-time U.S. stock sale by a foreign company in history and the third-largest IPO globally, behind only the Saudi Aramc offering and a small handful of Chinese state-owned bank listings. The structure of the deal, using ADRs rather than a direct primary listing, is a deliberate choice that allows SK Hynix to maintain its primary listing in Seoul while adding a deep, parallel liquidity pool in New York. The ADR ratio of one-tenth of a Korean share is also designed to keep the per-ADR price accessible to retail and to align with U.S. trading conventions.

What the Proceeds Will Fund

SK Hynix has signaled that the proceeds will be deployed in three buckets. The first is capacity expansion at the company’s Pyeongtaek and Cheongju fabrication facilities, where new clean rooms are being fitted out to produce next-generation HBM4 and HBM4E memory. The second is research and development on HBM5, the generation that will power the AI accelerators shipping in 2028 and 2029. The third is a partial deleveraging of the balance sheet, which has expanded as the company has front-loaded capital expenditure to keep pace with demand.

The investment cycle matters. The HBM market is currently supply-constrained, and the marginal capacity coming online in 2026 and 2027 is almost entirely pre-sold under long-term agreements with Nvidia, AMD, and the hyperscalers. By funding the next round of capacity expansion now, SK Hynix is positioning itself to be the dominant supplier in the 2027 to 2029 window, when AI training clusters are expected to scale by another order of magnitude.

Implications for the AI Supply Chain

For the broader AI ecosystem, the SK Hynix listing is more than a financial event. It is a public market validation of the AI memory thesis. The fact that the company could price its offering at a premium to the Korean market price, in the largest first-time U.S. sale by a foreign company in history, tells the market that the AI buildout is not a temporary cycle. It is a structural shift in computing demand, and the memory layer is one of the highest-conviction ways to play it.

For Nvidia, AMD, and the hyperscalers, the SK Hynix listing is also strategically reassuring. A well-capitalized, public-market-validated memory supplier is exactly the kind of partner the AI ecosystem needs. Memory shortages have been a recurring risk to the AI rollout over the past two years, and the SK Hynix capital raise reduces the probability of that risk materializing again. The Nasdaq debut, expected to begin trading within days, will be one of the most-watched listings of 2026, and a successful aftermarket performance will reinforce the AI capital cycle for the rest of the year.