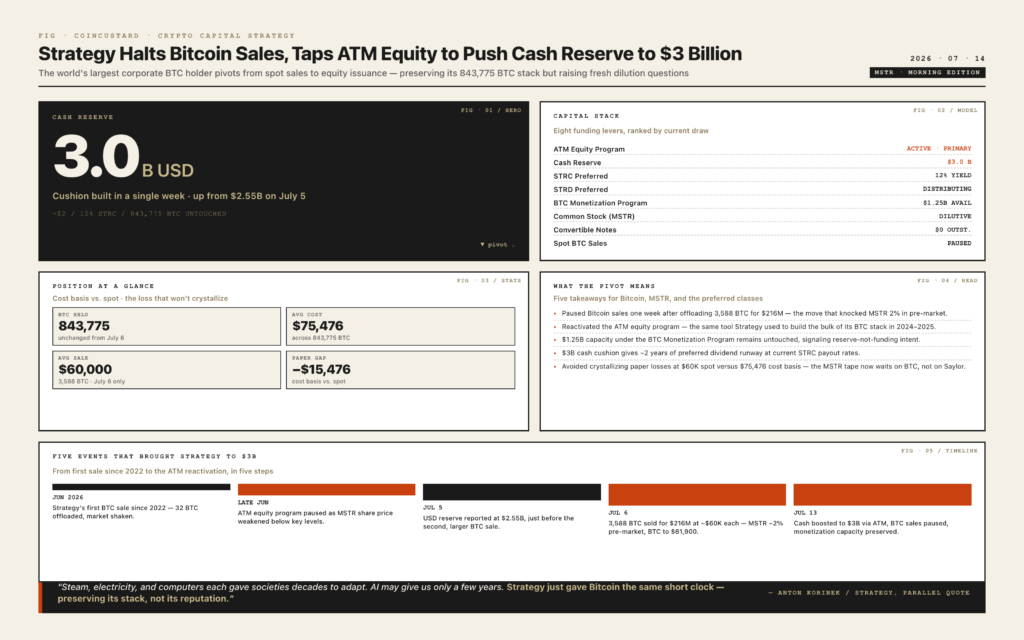

Strategy, the world’s largest corporate holder of Bitcoin, has paused its crypto sales and is now drawing on an older capital-raising tool to push its cash reserve to $3 billion, in a sharp tactical pivot that signals the company is no longer willing to part with its Bitcoin to fund dividend payments. The move, disclosed in a regulatory filing on Monday, comes just a week after Strategy sold 3,588 Bitcoin for $216 million to cover distributions on its preferred stock, an episode that knocked the share price and prompted renewed scrutiny of the company’s financing model. The latest reversal suggests the company is now prepared to lean on equity issuance rather than spot Bitcoin sales to keep its preferred dividends flowing, a structure that preserves the underlying crypto treasury but raises new questions about dilution and the cost of staying long.

Strategy, the software company rebranded from MicroStrategy under founder Michael Saylor, currently holds 843,775 Bitcoin acquired for approximately $63.69 billion, or an average price of $75,476 per coin. The company’s full $1.25 billion capacity under its recently announced Bitcoin Monetization Program remains untouched, a notable change from the previous week, when Strategy was actively drawing on that program to fund its STRC and STRD preferred dividend obligations. By switching the funding source, Strategy is choosing to preserve its crypto position at the cost of issuing new common stock, a trade-off that has been at the center of the bull-and-bear debate over the stock for the past two years.

The Cash Cushion and Why It Matters

The fresh $3 billion cash position, up from $2.55 billion on July 5, gives Strategy roughly two years of runway for its preferred dividends at current payout rates, based on the company’s most recent disclosures. That buffer is important because Strategy’s preferred classes, particularly STRC and STRD, have become a significant portion of the equity story. STRC, the flagship variable-rate preferred, currently offers a 12 percent headline yield, a level that the company can only sustain if it can keep paying distributions in cash, in stock, or in a combination of both. A longer cash runway reduces the risk of an in-kind distribution, which would dilute common shareholders and remove one of the more attractive features of the preferreds.

The decision to fund that runway through the older capital tool rather than spot Bitcoin sales is a deliberate choice about what the company is signaling to the market. Spot sales of Bitcoin by Strategy have consistently been read as a soft top signal, and the July 6 sale was no exception, with Bitcoin giving back much of its weekend gain and trading down to $61,900 from $62,900 in the hours after the announcement. The MSTR share price, which is highly correlated with Bitcoin spot price action, fell roughly 2 percent in pre-market trading that morning. By contrast, equity issuance has become almost routine for Strategy over the past three years, and the market has learned to price it in.

What the Old Funding Source Is

Strategy’s “old funding source” is its at-the-market (ATM) equity offering program, the same tool the company used to build the bulk of its Bitcoin position in 2024 and 2025. Under the program, Strategy sells common stock directly into the open market at prevailing prices, with the proceeds earmarked for additional Bitcoin purchases, working capital, and, more recently, preferred dividend funding. The program was paused briefly in late June as the share price weakened, but it has been the workhorse of Strategy’s capital strategy since the company began treating its balance sheet as a Bitcoin proxy. The pivot back to the ATM is, in effect, an admission that the Bitcoin Monetization Program is a reserve instrument, not a steady funding source.

What It Means for Bitcoin

For Bitcoin itself, the implications are mixed. On the positive side, Strategy is no longer a marginal seller into a market that has been range-bound for several weeks. The pause removes one of the more visible sources of supply pressure, even if the volumes involved were modest compared with overall spot market liquidity. On the negative side, Strategy is also no longer a marginal buyer through the ATM-and-Bitcoin cycle, which was the dominant source of incremental demand for several quarters. If the company is now sitting on cash, waiting for a better entry, the marginal-buyer story that supported prices through much of 2024 and 2025 becomes more complicated.

The Bigger Picture

Strategy’s recent behavior is best read as a company that is trying to preserve optionality rather than express a directional view. By holding the Bitcoin treasury intact and funding dividends through equity, the company is signaling that it remains committed to the long-term Bitcoin thesis, but that it is unwilling to crystallize losses on its stack in the current price environment. With Bitcoin trading at roughly $60,000 and Strategy’s average cost basis of $75,476 well above that, every spot sale is an acknowledgment of paper losses. The cash cushion gives the company the breathing room to ride out another quarter or two of price weakness without having to make that acknowledgment. For the rest of the market, the message is that the largest corporate Bitcoin treasury in the world is now in defense mode, and the next big move is likely to come from the price chart, not from the Strategy balance sheet.