Microsoft has begun replacing OpenAI and Anthropic models with its own in-house MAI artificial intelligence across Excel, Outlook, and the 365 Copilot suite, ending a years-long dependence on the two largest U.S. AI labs and marking the most aggressive step yet in Microsoft’s effort to capture the economics of generative AI for itself. The transition, first reported in early July 2026, turns the world’s largest productivity software vendor into a direct competitor to the same companies whose models have powered its flagship products since 2023.

The decision closes a strategic loop that Microsoft has been building for more than a year. At its June Build conference, the company unveiled a new generation of MAI models that, in internal benchmarks, match or surpass the capabilities of leading third-party systems while costing a fraction of the per-token price. Inside Microsoft, executives framed the rollout as a cost-control imperative as much as a performance upgrade. Heavy Copilot users on the company’s $200-per-month premium tier were generating compute bills of up to $14,000 per month, a unit-economics problem that no productivity vendor can sustain at scale. Replacing the underlying model is the cleanest way to claw that back.

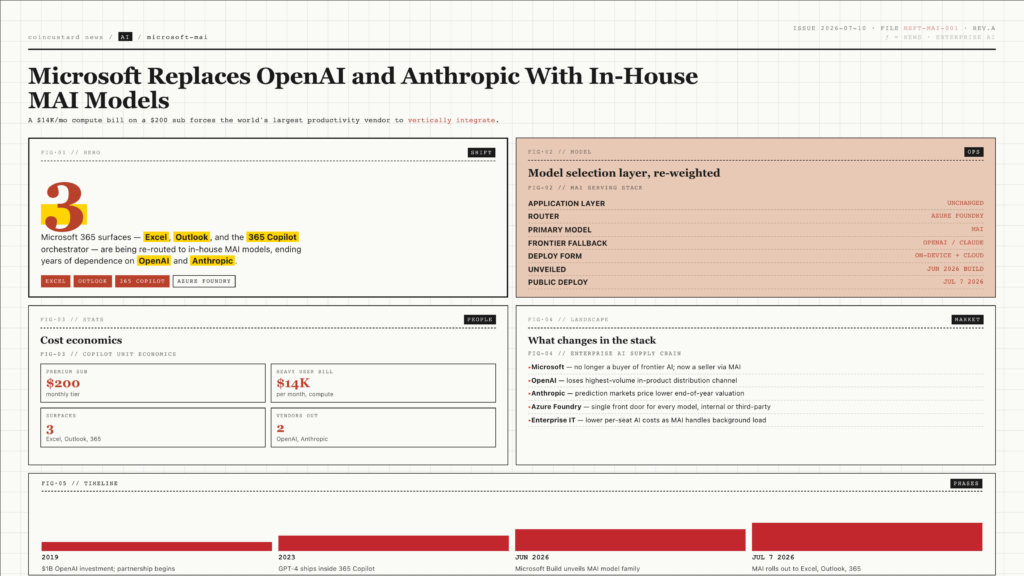

What Microsoft Is Replacing

The initial wave of model swaps covers the three Microsoft 365 surfaces where AI traffic is densest. Excel now runs MAI for formula generation, natural-language data analysis, and the new Python-in-cell agent. Outlook routes email summarization, reply drafting, and meeting-prep suggestions through Microsoft-built models. The 365 Copilot orchestrator, which dispatches tasks across the suite, is being retooled to prefer MAI unless a workload explicitly requires a frontier capability only the third-party labs can deliver.

Behind the scenes, the deployment is anchored on Azure Foundry, Microsoft’s model-serving platform, which lets the company route workloads across MAI, OpenAI, and Anthropic through a single API surface. That flexibility is what makes the swap practical: the application code is not being rewritten. The model selection layer underneath is being re-weighted. Microsoft can move workloads back to OpenAI or Anthropic the moment a specific use case demands it, and the company has stressed that frontier access to those providers remains intact for research, GitHub Copilot, and select enterprise contracts.

The Cost Story Behind the Swap

The economic argument is the most important part of the story and the least visible to end users. Frontier model inference is dominated by a handful of fixed costs: GPU hours, memory bandwidth, electricity, and the engineering overhead of serving low-latency requests at scale. Microsoft’s own data suggests that MAI handles a significant share of common Copilot tasks at materially lower marginal cost than the third-party models it is replacing. For a workload like Outlook email summarization, where prompts are short and outputs are highly templated, the cost gap between a frontier model and a well-tuned in-house alternative is largest.

That gap is what makes the swap commercially defensible. Microsoft is not betting that MAI is universally better than GPT-5 or Claude. It is betting that for the 80 percent of Copilot traffic that does not need absolute frontier capability, the company can deliver acceptable quality at a unit cost that keeps the $20 and $200 Copilot price points intact while protecting margins. The remaining 20 percent, the most demanding reasoning, coding, and scientific workloads, continues to run on the best external models Microsoft can buy.

What It Means for OpenAI and Anthropic

The shift arrives at an awkward moment for both of the companies being displaced. OpenAI is in the middle of a major enterprise push with its GPT-5.6 family, the same generation that Microsoft itself distributed for two years under the Copilot brand. Losing the inside of Microsoft 365 to an in-house competitor removes one of the highest-volume distribution channels for OpenAI’s models and puts pressure on a partnership that has been the foundation of OpenAI’s commercial revenue since 2023.

Anthropic, the more recent Microsoft partner, faces the sharper near-term impact. The company’s models were integrated into 365 Copilot and several enterprise products in 2025 to give Microsoft a hedge against OpenAI dependency. Prediction markets tracked a sharp move in Anthropic’s implied valuation outlook after the swap was reported, with traders pricing in lower confidence that Anthropic will reach its high-end December 2026 valuation target. Anthropic has so far declined to comment on the displacement beyond reaffirming that its broader enterprise pipeline remains intact.

Microsoft is no longer a buyer of frontier AI. It is a seller. That is the single most important shift in the enterprise AI market since OpenAI launched ChatGPT in 2022.

The Next Phase of the AI Stack

For the broader AI ecosystem, the most consequential effect of the Microsoft swap is what it signals about the maturity curve of the technology. Three years into the generative AI boom, the largest cloud vendor in the world is asserting that the underlying models have become commoditized enough to be built, served, and priced in-house. That is the same transition the database market made in the 2000s and the cloud object-storage market made in the 2010s, and it tends to be followed by a wave of consolidation, downward pricing pressure, and a scramble to differentiate at the application layer rather than the model layer.

For Microsoft customers, the practical impact of the MAI transition will be subtle in the short term and substantial over the next year. Excel and Outlook users will see faster responses, more consistent formatting, and a tighter integration with native Microsoft data types. Enterprise IT teams will see lower per-seat AI costs as MAI handles more of the background load. And developers building on Azure will see Microsoft lean harder on Foundry as the single front door for every model the company serves, whether built in Redmond, San Francisco, or anywhere else. The era of Microsoft as a neutral AI distributor is ending. The era of Microsoft as a vertically integrated AI vendor has begun.