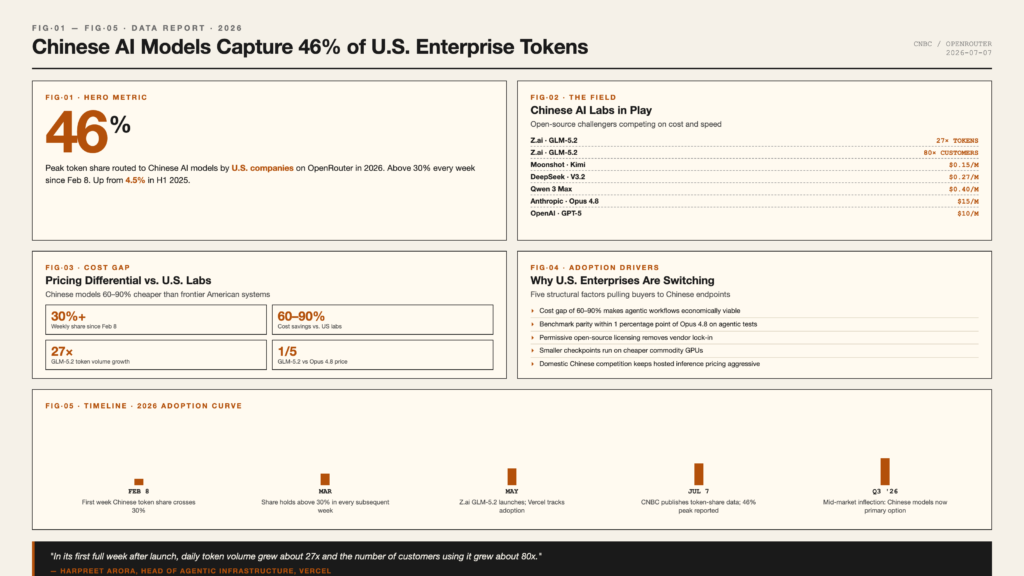

The share of AI compute flowing from United States companies to Chinese-built models has climbed above 30 percent every single week since February, peaking at 46 percent, according to new data from OpenRouter, the marketplace that lets developers mix and match competing model providers. The shift is the clearest signal yet that the cost gap between top-tier American and Chinese AI systems has reached a tipping point for enterprise buyers, with price differentials large enough to override lingering concerns about capability, data residency, and geopolitical risk.

In the first half of 2025, Chinese models accounted for just 4.5 percent of token traffic on the platform. Their share averaged 11 percent across the twelve months preceding the recent surge. The jump from 11 percent to a 46 percent peak in roughly seven months reflects how aggressively pricing has diverged between the two ecosystems as Chinese labs ship more efficient checkpoints and American labs keep raising prices on flagship tiers.

Price Gap Drives Adoption

OpenRouter data and analytics specialist Justin Summerville said the price differential is now stark. Open-source Chinese models run between 60 percent and 90 percent cheaper than their top American counterparts from Anthropic and OpenAI. For cost-sensitive enterprise buyers running high-volume inference workloads, that gap is the difference between a pilot project and a production deployment. It also determines whether an agentic workflow is economically viable at all, since many multi-step agent runs can consume thousands of tokens per task.

Among recent Chinese releases, GLM-5.2 from Beijing-based Z.ai has made the biggest splash in 2026. Harpreet Arora, head of agentic infrastructure at Vercel, told CNBC the model outpaced every other model Vercel tracked in 2026 on speed of adoption. Daily token volume grew roughly 27 times in the model’s first full week after launch, while the number of customers using it grew about 80 times. That adoption curve is faster than any frontier U.S. model release Vercel has hosted over the past 18 months.

Benchmark Performance at Fraction of the Cost

Performance parity is now close enough to make the cost gap decisive. On a prominent agentic benchmark, Z.ai’s GLM-5.2 finished within one percentage point of Anthropic’s Opus 4.8 while carrying a price tag approximately one-fifth as large. For enterprise teams running thousands of tool-using workflows daily, the math increasingly favors Chinese models even when raw capability is slightly lower.

The migration is happening across industries. LaunchLemonade, an AI agent platform focused on age verification, has shifted a meaningful portion of its traffic to Chinese endpoints. Smaller startups building agentic customer support tools have followed, citing both sticker price and the cost predictability of fixed-rate API contracts versus per-token billing on premium American tiers. Larger enterprises in finance and retail are also piloting Chinese models for non-sensitive workloads like content moderation, document summarization, and internal search.

“In its first full week after launch, daily token volume grew about 27x and the number of customers using it grew about 80x.” – Harpreet Arora, Vercel

Strategic Implications for U.S. AI Labs

The shift puts pressure on the dominant American labs in a new way. OpenAI and Anthropic have spent the past two years competing on raw capability, with each new flagship model leapfrogging the previous one on reasoning, coding, and long-context benchmarks. The new battleground is unit economics, and the economics of frontier inference have moved against the leaders.

If Chinese open-source models continue closing the capability gap while remaining a fraction of the price, American labs will need to either accept lower per-token margins at scale or accelerate moves toward smaller, more efficient models that can compete on cost as well as quality. The release cadence of distilled variants and the roll-out of aggressive enterprise pricing tiers suggest both paths are now being pursued simultaneously. OpenAI’s smaller GPT-5 mini tier and Anthropic’s Haiku refresh are the most visible examples.

What the Token Numbers Actually Show

The OpenRouter data captures developer behavior across thousands of production applications, making it one of the most reliable signals of which models real workloads are actually running on. Token consumption is the cleanest proxy for usage volume, and the sustained 30 percent-plus weekly share for Chinese models suggests this is not a transient spike tied to a single launch.

Three structural factors keep the gap wide. First, Chinese labs have prioritized training efficiency and model distillation, producing smaller checkpoints that run on less expensive hardware. Second, open-source licensing under permissive terms removes vendor lock-in and lets enterprises self-host if data residency requires it. Third, aggressive pricing on hosted inference endpoints reflects domestic competitive pressure in China’s crowded model market, where Z.ai, Moonshot, DeepSeek, and Qwen all compete for the same enterprise buyers.

The Mid-Market Inflection Point

The cost dynamics matter most for the mid-market segment. Large enterprises with deep engineering teams can still afford to pay premium prices for the highest-capability models, while startups running lean infrastructure have always chased the cheapest viable option. The middle tier, companies with real budgets but sharp efficiency mandates, is where the Chinese model share has grown fastest. For these buyers, the choice is now between two to three times the inference quality at eight to ten times the price, and the value calculation has shifted decisively toward cost.

Outlook

The cost-versus-capability curve is reshaping the enterprise AI stack faster than the frontier-model headlines suggest. For U.S. enterprises running high-volume inference, Chinese models are no longer a curiosity or a fallback. They are a primary option. For American labs, the path forward runs through efficiency gains, sharper distillation, and pricing innovation. Chinese AI models have moved from experimental to essential in the enterprise inference mix, and the share will likely climb further before it stabilizes into a new equilibrium that defines the AI cost stack for the rest of the decade.