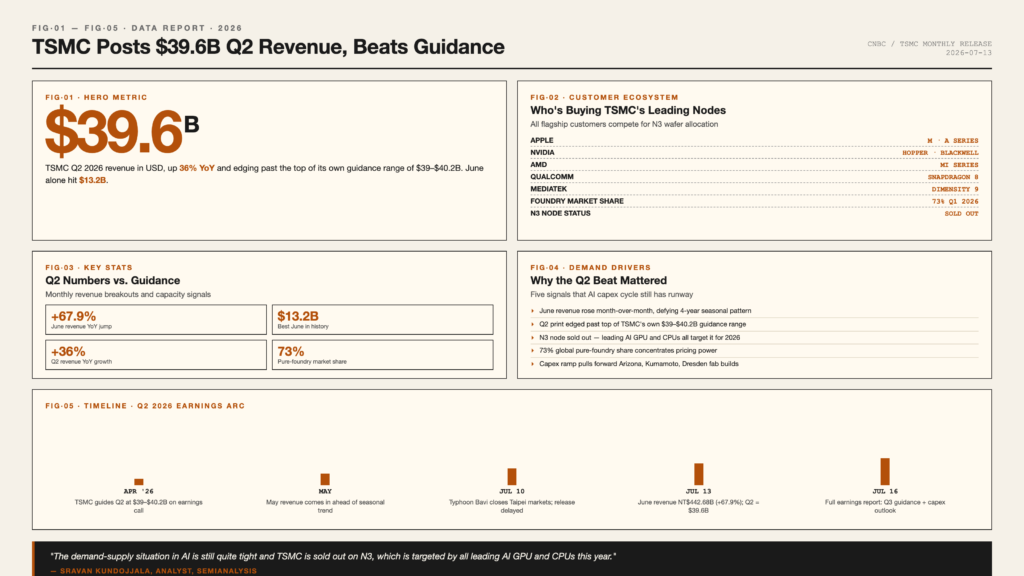

Taiwan Semiconductor Manufacturing Co. reported record June revenue of 442.68 billion New Taiwan dollars, roughly 13.2 billion U.S. dollars, capping a second quarter that exceeded the chipmaker’s own guidance range. The figures, delayed by a typhoon that shuttered Taipei’s financial markets, reinforce the view that AI chip demand is still running well ahead of supply across the most advanced process nodes.

June sales jumped 67.9 percent from the same month a year earlier and rose 6.2 percent from May, marking the best month in TSMC’s history. The print lifted the chipmaker’s second-quarter revenue to 1.27 trillion New Taiwan dollars, approximately 39.6 billion dollars, a 36 percent increase from the same period in 2025 and a number that would have seemed unrealistic just three years ago when quarterly revenue was running closer to 20 billion dollars.

Guidance Beat and N3 Sellout

TSMC’s Q2 result edged past the top of its own guidance range of 39 billion to 40.2 billion dollars, which the company issued during its April earnings call. Sravan Kundojjala, an analyst at SemiAnalysis, called the numbers quite robust and noted that June revenue rising month over month runs counter to the seasonal pattern of the past four years. Semiconductor cycles typically show sequential declines between May and June as customers burn through inventory built up earlier in the year.

The more important signal is the supply situation on the N3 node. Kundojjala said the demand-supply balance in AI is still quite tight and that TSMC is sold out on N3, which is the process node targeted by all leading AI GPUs and CPUs scheduled for release this year. A sold-out node means TSMC has little short-term flexibility to add capacity even if a customer wants more wafers, which translates directly into pricing power and backlog visibility.

Foundry Market Dominance

TSMC commands a 73 percent share of the global pure-foundry market as of the first quarter of 2026, according to data from Counterpoint Research cited by CNBC. The market share figure matters because it captures the company’s grip on advanced process manufacturing, where most AI accelerators, smartphone system-on-chips, and high-performance computing parts are produced. No other foundry operates at the same scale on the leading edge.

Foundry market share at 73 percent gives TSMC pricing power that few semiconductor manufacturers can match. The company’s customers include Apple, Nvidia, AMD, Qualcomm, and MediaTek, all of which depend on TSMC’s most advanced nodes for flagship products. With alternative foundries either one node behind or focused on specialty processes, the leading customers have very limited ability to dual-source their most advanced designs.

“The demand-supply situation in AI is still quite tight and TSMC is sold out on N3.” – Sravan Kundojjala, SemiAnalysis

Typhoon Delay and Stock Reaction

Publication of the monthly revenue figures had been scheduled for last Friday, but Typhoon Bavi forced the closure of Taipei’s financial markets, pushing the release to Monday. Despite the unusual timing, the print was clean and the stock reacted with a measured advance. TSMC’s Taipei-listed shares closed up 1 percent on Monday ahead of the data’s release, reflecting relief that the delayed numbers did not contain any unexpected weakness.

The monthly revenue release contained no additional commentary or outlook, leaving investors to wait for Thursday’s full earnings report for color on Q3 guidance, capital expenditure plans, and the pace of N3 and N2 capacity additions. That earnings call will be the next major catalyst for the stock and for the broader semiconductor sector, since the capex number will reveal how aggressively TSMC is pulling forward new fab construction in Arizona, Kumamoto, and Dresden.

What an N3 Sellout Means for AI Hardware

Sold-out N3 capacity has direct implications for the AI hardware supply chain. Nvidia’s upcoming accelerator generations, AMD’s MI series, and Apple’s M-series and A-series chips all rely on TSMC’s most advanced nodes. When the foundry is sold out, customers compete for allocation rather than negotiate price, and the upstream supply of high-bandwidth memory, advanced packaging, and substrate capacity becomes the binding constraint on how much AI silicon can actually ship in any given quarter.

The N3 sellout also signals that demand for AI training and inference silicon has not cooled despite periodic concerns about an infrastructure bubble. Customers booking N3 capacity in 2026 are committing to designs that will ship in 2027 and beyond, suggesting that the AI capex cycle still has multiple years to run. The implications extend beyond chipmakers to memory suppliers like SK Hynix and Micron, packaging partners, and the broader power and cooling infrastructure build-out required to support larger AI data centers.

Advanced Packaging as the Next Bottleneck

CoWoS, TSMC’s chip-on-wafer-on-substrate advanced packaging technology, has emerged as the single biggest constraint on AI accelerator shipments in 2025 and 2026. The capacity expansion for CoWoS lines, particularly the move from CoWoS-S to CoWoS-L configurations, is closely watched by analysts because it determines how many high-end AI chips can be assembled regardless of how many wafers TSMC produces. Continued N3 sellouts suggest that even a successful packaging ramp will leave TSMC supply-constrained through at least the first half of 2027.

Outlook

TSMC Q2 revenue delivered a clear message. AI chip demand remains tight, the foundry market is concentrating further around the leading manufacturer, and the seasonal patterns that typically govern semiconductor cycles are being overridden by the structural pull from AI infrastructure. Thursday’s full earnings report will show whether the second half of 2026 keeps the same trajectory or whether customers are starting to digest capacity. For now, the TSMC Q2 revenue beat is the strongest evidence yet that the AI buildout is still in its expansion phase and that the supply chain remains sold out on the most advanced nodes that the industry depends on.