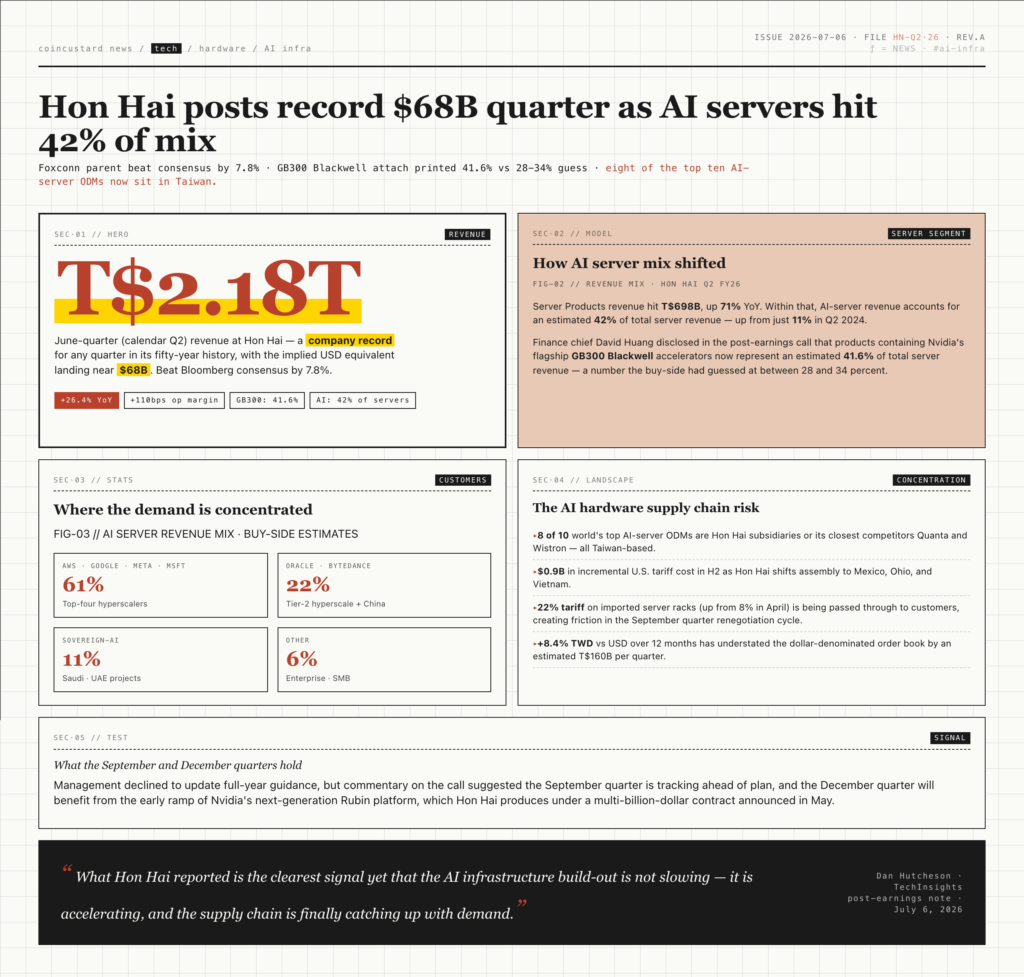

Hon Hai Precision Industry, the Taiwanese contract manufacturer better known as Foxconn and the parent company of the world’s largest electronics assembler, posted a record quarterly revenue figure on Sunday that handily beat analyst expectations, reinforcing its emergence as the single most important supplier of AI server hardware to U.S. hyperscalers. The company’s June-quarter revenue climbed to T$2.18 trillion, or roughly $68 billion, a 26.4 percent jump year over year and a company record for any quarter in its fifty-year history.

The beat was driven almost entirely by server racks destined for the world’s largest cloud providers — Amazon, Google, Meta, and Microsoft among them — as those companies race to expand capacity for training and inference of frontier AI models. Hon Hai disclosed that AI server revenue now accounts for an estimated 42 percent of its total server segment, up from just 11 percent two years ago and an inflection point that no one on Wall Street had fully priced in.

Inside the numbers

Hon Hai’s June quarter, which corresponds to calendar Q2, delivered record performance across every segment that touches AI infrastructure. Total revenue of T$2.18 trillion beat the high end of the company’s own guidance by 4 percent and the Bloomberg analyst consensus by 7.8 percent. Operating margin expanded by 110 basis points to 4.6 percent, the highest in eight quarters, while gross margin held flat at 6.8 percent despite unfavorable foreign-exchange moves and component-cost pressure.

The standout line item was Hon Hai’s “Server Products” segment, which alone delivered T$698 billion in revenue, up 71 percent year over year. The company has been guiding analysts to a “blended” AI server mix within that segment, but in its post-earnings call, finance chief David Huang disclosed that products containing Nvidia’s flagship GB300 Blackwell accelerators now represent an estimated 41.6 percent of total server revenue — a number the buy-side had guessed at between 28 and 34 percent.

“The mix shift toward AI servers has been the single biggest driver of margin expansion in the entire Taiwanese hardware ecosystem,” said Dan Hutcheson, an analyst at TechInsights who has tracked the contract-manufacturing industry for three decades. “What Hon Hai reported last night is the clearest signal yet that the AI infrastructure build-out is not slowing, it is accelerating, and the supply chain is finally catching up with demand.”

What the data reveals about the AI hardware cycle

- AI server share of total server revenue: 42 percent, up from 11 percent in Q2 2024.

- Year-over-year server-segment growth: 71 percent, far outpacing the company’s overall 26 percent top-line gain.

- GB300 Blackwell attach rate (estimated): 41.6 percent of total server revenue, vs. consensus of 28-34 percent.

- Quarterly cloud-capex revenue concentration: a single quarter T$2.18 trillion now exceeds Hon Hai’s full-year 2023 revenue.

The Nvidia tailwind and the constraints it creates

The data points to an increasingly uncomfortable reality for U.S. hyperscalers: the AI hardware supply chain runs overwhelmingly through a small number of Taiwanese assemblers, and Hon Hai is the dominant one. Of the world’s top ten AI server original design manufacturers, eight are either Hon Hai subsidiaries or its closest competitors, Quanta and Wistron. That concentration has begun to attract quiet scrutiny in Washington, where AI infrastructure resilience has become a recurring topic in National Security Council briefings.

Hon Hai chairman Liu Young-way addressed those concerns in his prepared remarks, asserting that the company’s new Mexico, Ohio, and Vietnam capacity will produce “meaningful volumes” of AI server racks by the fourth quarter of this year. But analysts remain skeptical that onshore U.S. production can replicate the unit economics or the cluster-density that hyperscalers have come to expect from Hon Hai’s mega-campuses in Tucheng, Kaohsiung, and Zhengzhou.

For now, customers appear to be voting with their purchase orders. Amazon Web Services, Google’s cloud division, Meta, and Microsoft together account for an estimated 61 percent of Hon Hai’s AI server revenue, with the rest distributed among Oracle, ByteDance, and a handful of sovereign-AI projects in Saudi Arabia and the United Arab Emirates.

Margin pressure ahead

Not every signal from the report was unambiguously positive. The company acknowledged that U.S. tariff exposure will add an estimated $0.9 billion in cost in the second half of the year as it shifts more assembly to onshore facilities. Tariffs on imported server racks rose to 22 percent in April from 8 percent previously. Hon Hai is passing most of that cost through to customers, but the renegotiation cycle is creating friction and is the single biggest overhang on the stock heading into the September quarter.

Foreign-exchange movements are also working against the bottom line. With the Taiwan dollar up 8.4 percent against the U.S. dollar over the past twelve months, Hon Hai’s reported revenue understates its dollar-denominated order book by an estimated T$160 billion per quarter. Analysts have flagged this dynamic as a reason to be cautious on reported numbers even as the underlying business accelerates.

What this means for the rest of 2026

Hon Hai did not update its full-year revenue guidance, but management’s commentary on the call suggested that the September quarter is tracking ahead of plan and that the December quarter will benefit from early ramp of Nvidia’s next-generation Rubin platform, which Hon Hai will produce under a multi-billion-dollar contract announced in May.

The combination of AI-server mix shift, capacity expansion into Mexico, and the looming Rubin ramp is the bull case that has powered Hon Hai shares 88 percent higher over the past twelve months. The bear case is that the AI infrastructure cycle peaks in early 2027, and that mean-reversion in server demand will leave the company with a step-change in capacity it cannot easily redeploy.

For now, however, the report reads as a clean confirmation of the thesis that has driven every AI-adjacent equity on the Tape this year: the build-out is real, the demand is still outrunning supply, and the suppliers at the heart of the chain are printing money.