Global startup investment hit a record $510 billion in the first half of 2026, with the AI boom pulling in more than two-fifths of all venture dollars, according to fresh data from Crunchbase News. The figure underscores how a handful of frontier model labs is now dictating the pace and direction of private capital markets worldwide.

The $510 billion total for H1 2026 marks the strongest six-month stretch ever recorded in venture history. Investors poured more than $200 billion into startups globally in the just-ended Q2 2026 alone, making it the second-largest quarter on record. The first quarter had already shattered records at $300 billion, meaning that even as the pace cooled from January through March, capital deployment stayed near historic highs through April, May and June. According to the data, four of the five largest venture rounds ever recorded closed in Q1 2026, led by OpenAI at $122 billion and Anthropic at $30 billion, followed by xAI at $20 billion and a major autonomous-driving player.

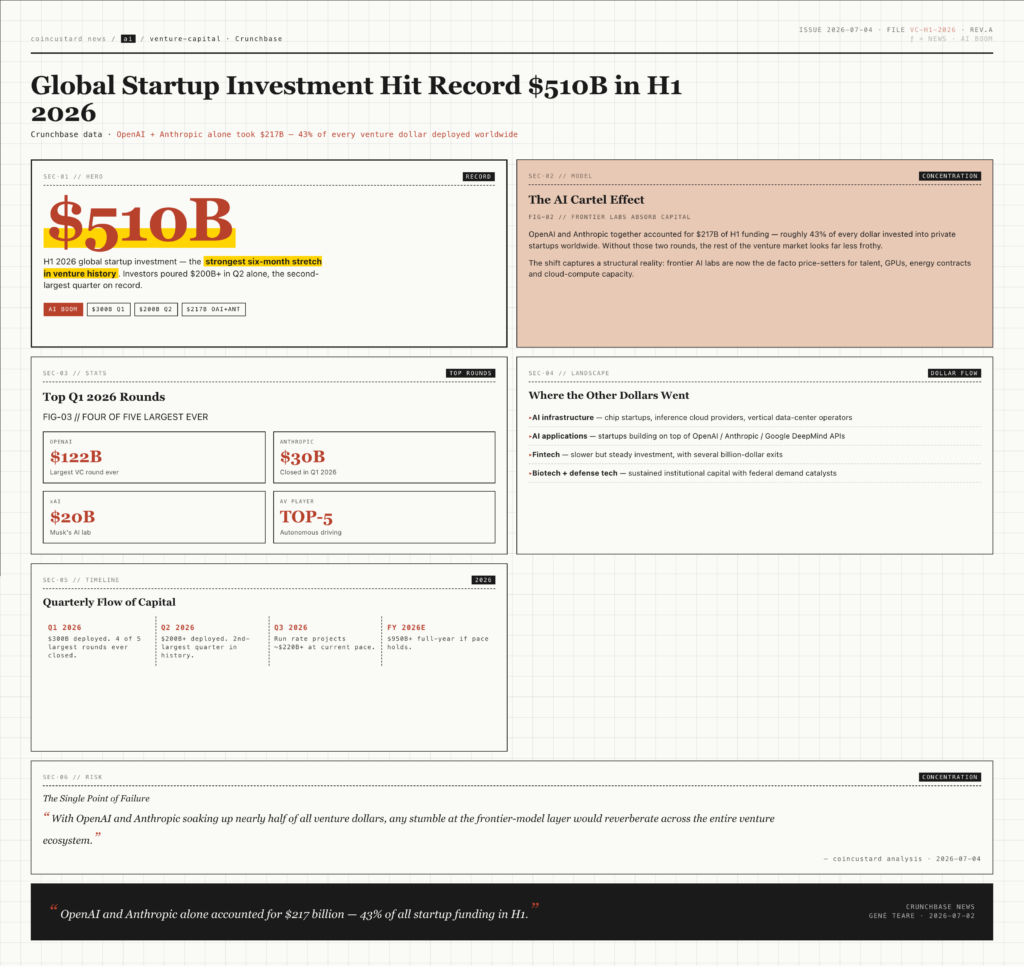

The AI Cartel Effect

OpenAI and Anthropic alone accounted for $217 billion of the H1 2026 total, which works out to roughly 43 percent of every dollar invested into private startups worldwide in the first half. That single statistic captures the structural shift in venture markets: capital is concentrating at the frontier-model layer faster than at any previous point in the industry’s history.

Strip out those two companies and the broader venture market would look far less frothy. The aggregate $510 billion total would shrink by more than 40 percent, and the narrative of a uniform startup boom would collapse into a story of two outlier rounds plus a steady but unspectacular middle market. The implication for founders, limited partners and policymakers is stark — frontier AI labs are now the de facto price-setters for talent, GPUs, energy contracts and even cloud-compute capacity, and every other category of startup is competing for the leftover pool.

Where the Other Dollars Went

Beyond the frontier-model giants, capital flowed heavily into AI infrastructure plays — chip startups, inference cloud providers and vertically integrated data-center operators. The data also tracks strong fundraising from AI application companies building on top of OpenAI, Anthropic and Google DeepMind APIs, as well as continued — though slower — investment in fintech, biotech and defense tech. Exit activity picked up sharply in Q2, with multiple billion-dollar acquisitions and a fresh batch of venture-backed IPOs that gave limited partners the distributions they had been waiting on since 2024.

What This Means for the Rest of 2026

If H1 closed at a $510 billion run rate, the full-year 2026 total could plausibly land north of $950 billion — a number that would have been unthinkable as recently as 2023, when annual venture funding struggled to clear $350 billion globally. The shift reflects three forces converging: corporate AI budgets that now routinely exceed nine figures per customer, hyperscaler demand for AI-specific GPUs that has spawned a parallel infrastructure industry, and a fundraising environment where top-tier AI founders can demand terms once reserved for late-stage public companies.

The risk for the rest of the year is concentration. With OpenAI and Anthropic soaking up nearly half of all venture dollars, any stumble at the frontier-model layer — a safety incident, a regulatory action, a public model release that disappoints — would reverberate across the entire venture ecosystem. Conversely, a single successful IPO from one of those two labs could trigger a second wave of distributions and recycling, fueling another $200 billion quarter in Q3 or Q4. For now, the venture industry is in uncharted territory, with the AI boom acting as both engine and single point of failure for the largest capital cycle the private markets have ever seen.

The Crunchbase analysis shows that frontier AI labs have become the dominant price-setters for talent, compute and capital across the entire venture industry.

The Application-Layer Squeeze

The flip side of the frontier-lab concentration story is what it means for the application layer — the thousands of startups building products on top of OpenAI, Anthropic and Google DeepMind APIs. Those companies are simultaneously the biggest beneficiaries of the model-price collapse and the most exposed to the concentration risk. If frontier labs continue to absorb their pricing power, the application layer will need to defend itself with proprietary data, deep workflow integration or distribution advantages that the model providers cannot easily replicate. The venture flows of H2 2026 will be the first major test of whether that defense holds — or whether the AI boom keeps funneling an outsized share of every dollar back to the same two or three names.

Exits Return, Distribution Returns

The other major H1 2026 story buried in the Crunchbase data is the return of exits. After two years of frozen IPO markets and depressed M&A activity, the second quarter saw a fresh wave of billion-dollar acquisitions and several venture-backed public listings that gave limited partners the distributions they had been waiting on. Strong exit activity is what allows venture funds to recycle capital back into new funds, which is what funds the next generation of startups. The combination of record investment on the front end and recovering exits on the back end is exactly the configuration that produces compounding boom cycles — and the data suggests 2026 is now firmly in that mode.