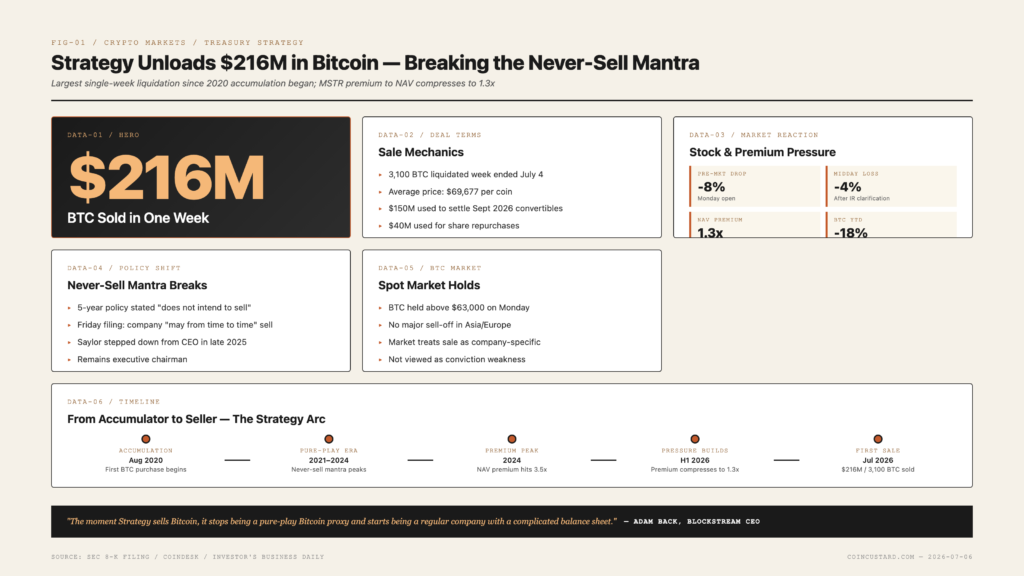

Michael Saylor’s Strategy dramatically accelerated the pace of its Bitcoin sales last week, offloading roughly $216 million worth of the cryptocurrency and breaking with the company’s long-standing “never sell” mantra that had been a cornerstone of its pitch to institutional investors. The disposals, disclosed in a regulatory filing late Friday, mark the largest single-week liquidation by Strategy (formerly MicroStrategy) since the company began its Bitcoin accumulation program in 2020, and sent MSTR shares tumbling in pre-market trading on Monday.

Strategy sold 3,100 BTC at an average price of approximately $69,677 per coin during the week ended July 4, according to the Form 8-K filed with the SEC. The sale generated roughly $216 million in net proceeds, which the company said would be used for general corporate purposes including debt service on its convertible notes. The disclosure comes against a backdrop of a roughly 18 percent year-to-date decline in Bitcoin’s price and growing pressure on Strategy’s stock, which trades at a substantial premium to the net asset value of its Bitcoin holdings.

Breaking the Never-Sell Mantra

For more than five years, Strategy’s pitch to investors rested on a simple promise: accumulate Bitcoin, never sell, and let shareholders ride the appreciation. Saylor personally became one of the most prominent corporate evangelists for the asset, appearing at conferences around the world and at one point personally holding more than $1 billion worth of Bitcoin on his personal balance sheet. The company’s official treasury policy, posted to its investor relations site, still states that Strategy “does not currently intend to sell any Bitcoin held by the company.”

Friday’s filing hedged that language for the first time, noting that the company “may from time to time” sell Bitcoin to meet obligations or manage liquidity. The shift in tone was enough to trigger a sharp reaction in the stock, which fell more than 8 percent in pre-market trading on Monday before paring losses after Strategy’s investor relations team issued a clarification that the sales were routine and did not represent a strategic reversal. By midday, MSTR was down roughly 4 percent on the session.

Pressure From a Squeezed Premium

Strategy’s stock has long traded at a premium to the value of its Bitcoin holdings — a gap that retail investors were willing to pay because of the company’s aggressive accumulation and the perception of Saylor as a Bitcoin oracle. That premium has compressed sharply in 2026 as Bitcoin’s price has stagnated and as more direct competitors, including spot Bitcoin ETFs, have made it easier for institutions to gain exposure without paying the corporate tax and structural overhead that comes with MSTR shares.

At Monday’s prices, the premium to NAV had narrowed to roughly 1.3x, down from a peak above 3.5x during the 2024 Bitcoin rally. Some short sellers had been positioning for the premium to compress to parity, and a major Bitcoin sale by the issuer itself accelerates that arbitrage. Analyst consensus has been calling for the company to issue additional convertible debt or sell equity to raise capital, both of which dilute the per-coin leverage that has been Strategy’s main attraction. Selling actual Bitcoin is a third option that until this week was considered off the table.

“The moment Strategy sells Bitcoin, it stops being a pure-play Bitcoin proxy and starts being a regular company with a complicated balance sheet. The premium collapse we’ve seen over six months is the market getting ready for exactly this event.” — Adam Back, CEO of Blockstream

What the Filing Reveals

The Form 8-K filed Friday contained several disclosures that broke from Strategy’s previous pattern. Beyond the headline sale of 3,100 BTC, the company disclosed that it had used approximately $150 million of the proceeds to settle a tranche of convertible notes coming due in September, and that it had repurchased roughly $40 million of its own shares during the week — an unusual move for a company that has historically been a serial equity diluter. The combination of Bitcoin sales, debt repayment, and share repurchases suggests a more defensive capital management posture than Strategy has signaled in any prior filing.

The filing also noted that the company’s average cost basis for its Bitcoin holdings now stands at roughly $66,300 per coin, slightly below the current market price. That is a sharp improvement from earlier in 2026, when the average cost basis was well above spot and the company was sitting on substantial paper losses. The recent rally from sub-$58,000 levels in May has brought Strategy back into profit on a mark-to-market basis for the first time in several months, giving it more flexibility to sell without crystallizing losses.

Implications for Bitcoin Itself

The Bitcoin market absorbed the news without a major sell-off. Spot BTC held above $63,000 in Asian and European trading on Monday, suggesting that institutional and retail buyers view Strategy’s sales as company-specific rather than a signal of broader conviction weakness. That interpretation aligns with the relatively narrow price impact during prior quarters when Strategy has trimmed positions on a much smaller scale. The market now treats the company as a price-sensitive actor rather than an infinite accumulator, a categorization Saylor has fought for years.

Looking ahead, Strategy’s next quarterly filing will be the most closely watched in years. Investors will be looking for guidance on whether the $216 million sale represents a one-off liquidity event or the start of a sustained period of disposals as the company manages an increasingly complex balance sheet. Saylor, who stepped down from the CEO role in late 2025 but remains executive chairman, is scheduled to appear at the Bitcoin 2026 conference in Nashville next month, where he will almost certainly be asked to explain the new chapter in the Strategy story.